Comparing CFDs vs Spread Betting is one of the most common questions from traders in the UK and Europe. Both are powerful leveraged products that allow you to trade on price movements without owning the underlying asset, but there are critical differences in tax, structure, and strategy.

In this guide, Piprider will break down these key distinctions in detail, helping you choose the right tool for your trading.

Key Takeaways

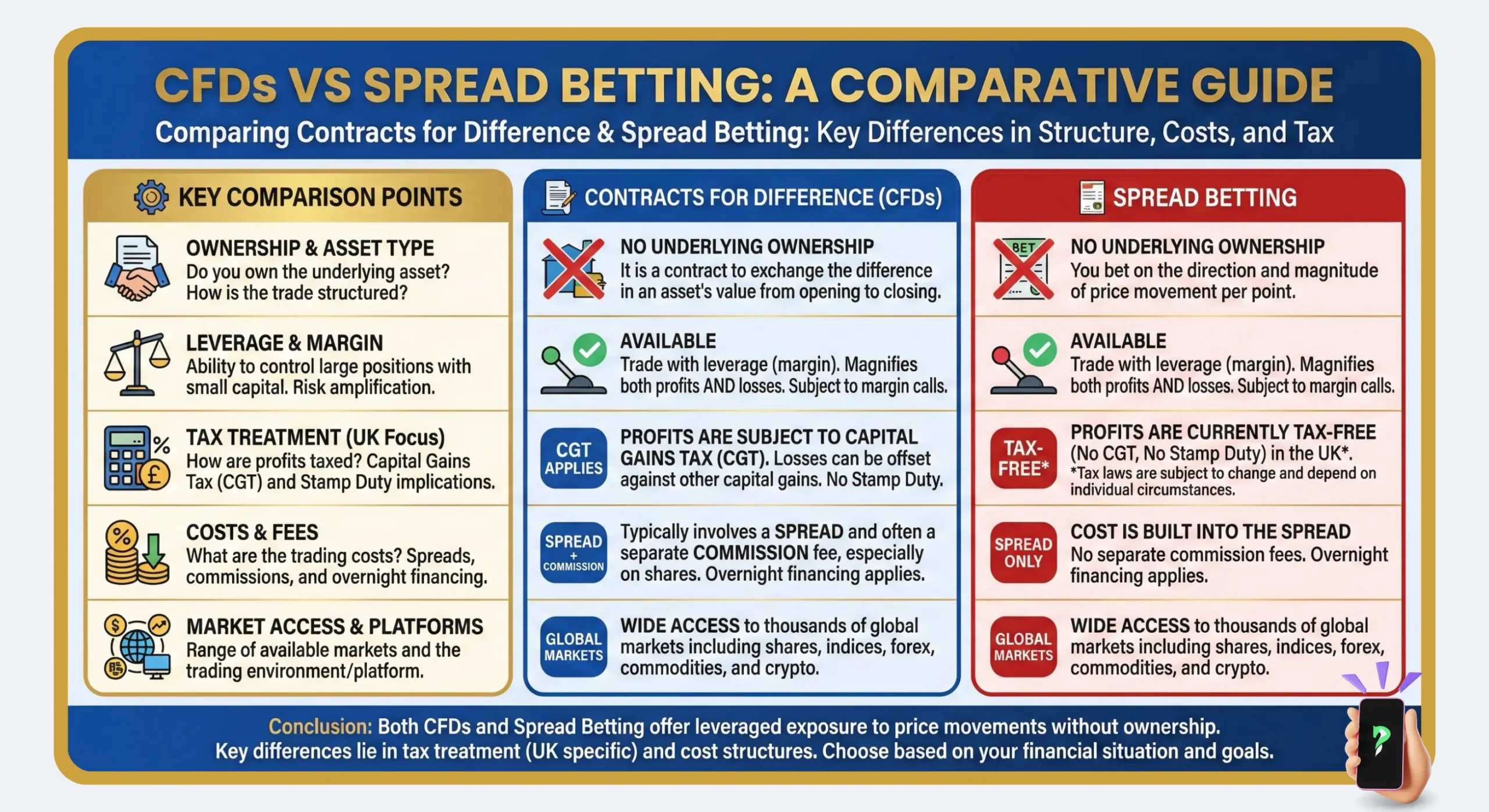

- CFDs (Contracts for Difference) and spread betting are both derivative contracts based on an asset’s price movements.

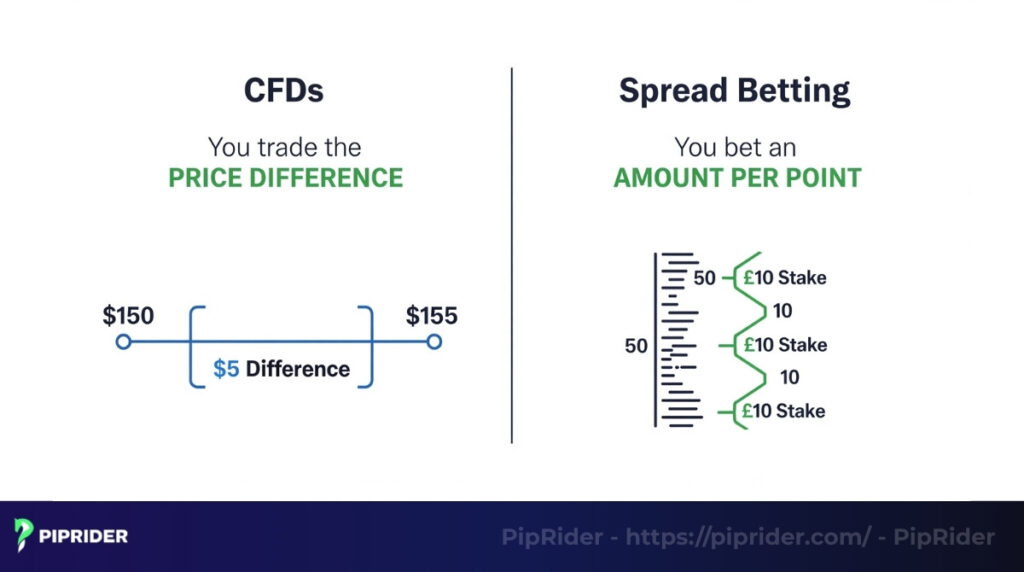

- With CFDs, you buy/sell contracts based on a price difference, and they are available in many global markets.

- With spread betting, you bet an amount per point of movement, and it is most popular in the UK & Ireland.

- Tax: In the UK, spread betting is often free from capital gains tax, while profits from CFDs are taxed, but losses may be deductible against future profits.

- The choice between these financial instruments depends on your location, trading goals, and the legal framework.

1. What Are CFDs and Spread Betting?

To understand the strategies, we first need to be clear on how these two powerful financial instruments work. While they share similarities, their core mechanics are distinct.

1.1. Understanding CFDs

A Contract for Difference (CFD) functions as a direct trading agreement established between a trader and a brokerage. Before diving into comparisons, mastering the fundamentals of CFD trading is essential for understanding how these derivatives allow participants to speculate strictly on an asset’s price trajectory (buying or selling) without ever taking physical ownership of the underlying instrument. Instead of transferring actual shares, this cash-settled mechanism simply exchanges the price difference recorded between the opening and closing of the trade (Investopedia, 2023).

In practice, operators directly choose to ‘buy’ (go long) to capture upward momentum, or ‘sell’ (go short) to profit from declines. Utilizing leverage means traders only deploy a small fractional deposit (margin) rather than funding the position’s full notional value. Final profit or loss calculations depend entirely on the price variance between the entry and exit points.

Practical Example (Forex CFD): An operator anticipates the EUR/USD will rise from 1.1000 to 1.1050. By purchasing 1 standard lot (100,000 units), the trader captures a 50-pip move. Each pip is valued at $10, resulting in a $500 gross profit. Conversely, a 50-pip drop results in an equivalent $500 loss, highlighting the linear relationship between price movement and contract value.

1.2. Understanding Spread Betting

Spread betting operates as a specialized form of financial speculation where traders place directional wagers on an asset’s price fluctuations without acquiring the physical asset. Market leaders like CMC Markets define this vehicle as a tax-efficient alternative to traditional investing, providing exposure to thousands of global instruments through a wagering mechanism rather than contract ownership (CMC Markets, 2024).

Securing profits through this specific vehicle offers a massive structural advantage: the returns often remain completely exempt from capital gains tax and stamp duty within the UK and Ireland (Investopedia, 2024). Regulatory oversight provided by the Financial Conduct Authority (FCA) ensures that these activities remain transparent, mandating that brokerages provide negative balance protection for all retail practitioners (FCA, 2024).

Instead of purchasing a specific number of shares or contract lots, participants simply risk a defined amount of currency for every incremental “point” the market moves. Industry professionals refer to this metric as the stake per point.

Calculating financial exposure and potential returns requires a straightforward mathematical framework. Operators determine their net outcome using this fundamental equation:

Realized Profit/Loss = (Stake per Point) × (Total Points Moved)

Practical Example (Spread Betting Mechanics): Consider a practitioner deploying capital on the UK100 index using a defined stake of £10 per point. The trader executes a long entry at an index level of 7500.

- Profit Scenario: The market advances to 7550, generating a favorable 50-point directional move. Multiplying the £10 stake by the 50 points yields a £500 tax-free return (subject to UK tax laws).

- Loss Scenario: Market structure breaks down, dropping the index to 7480 (a negative 20-point excursion). Multiplying the £10 stake by the 20-point drop results in a £200 realized loss directly debited from the account balance.

1.3. Key Similarities

While differing in mathematical construction, both instruments share fundamental characteristics that define modern derivative trading. Recognizing these parallels ensures practitioners understand why both are elite tools for capturing global market volatility.

| Core Feature | CFDs | Spread Betting |

|---|---|---|

| Asset Ownership | Speculative exposure only (No physical ownership) | Speculative exposure only (No physical ownership) |

| Market Direction | Bi-directional (Long and Short capabilities) | Bi-directional (Long and Short capabilities) |

| Leverage & Margin | High capital efficiency via fractional deposits | High capital efficiency via fractional deposits |

| Regulatory Caps (UK/EU) | Strict ESMA/FCA leverage limits applied | Strict ESMA/FCA leverage limits applied |

| Asset Versatility | Access to FX, Indices, Stocks, and Commodities | Access to FX, Indices, Stocks, and Commodities |

Gaining exposure to diversified markets without the logistical burden of physical asset delivery represents the primary advantage of these derivatives. Both vehicles empower operators to amplify potential returns through leverage, though this mechanism necessitates an advanced risk-management framework to mitigate the heightened probability of rapid capital depreciation.

2. Core Operational Differences: CFDs vs. Spread Betting

While both instruments allow practitioners to capitalize on directional market movements using leverage, their underlying mathematical structures and execution costs differ fundamentally.

2.1. Trade Mechanics and Structural Execution

Executing CFD positions strongly mimics traditional market participation. Operators purchase or sell a specific volume of standardized contracts representing the underlying asset. Finalizing the trade calculates the exact price differential between entry and exit, multiplying that figure by the total number of contracts held.

Conversely, spread betting discards the contract-based model entirely. Participants simply define a strict monetary wager (stake) assigned to every single point of price fluctuation. Operating this model means market exposure scales linearly based on the point-distance moved, rather than the intrinsic value of standardized contract lots.

2.2. Cost Structures and Financing Fees

Brokerage models extract revenue differently across these two derivative instruments, directly impacting short-term scalping versus long-term swing trading strategies.

Trading CFDs, particularly within global equity markets, typically provides access to institutional-grade tight spreads. However, securing these narrow spreads often requires paying explicit, separate commission charges per trade. Maintaining these leveraged positions beyond daily market closure also subjects the account to overnight financing fees (swaps), which can erode long-term profitability.

Spread betting incorporates the entire execution cost directly into the bid-ask spread. Utilizing this model completely eliminates separate commission charges, simplifying cost calculations for rapid execution. The primary trade-off requires practitioners to navigate slightly wider spreads compared to direct CFD pricing.

3. Tax Implications & Regulatory Frameworks

Navigating the legal and fiscal landscape remains the most critical factor when choosing between these two derivative classes. Jurisdictional laws strictly dictate both your profit retention and your operational boundaries.

3.1. The Tax Advantage: Capital Gains vs. Tax-Free Returns

Structuring your trading vehicle directly impacts your net profitability. In the United Kingdom and Ireland, spread betting enjoys a massive structural advantage: realized profits remain completely exempt from Capital Gains Tax (CGT) and stamp duty. Classifying these trades legally as “betting” rather than investing shields the returns from standard revenue collection (Investopedia, 2024).

Conversely, executing CFDs generates taxable income. Operators must declare CFD profits under standard Capital Gains Tax frameworks. However, trading CFDs offers a highly strategic offset mechanism: practitioners can legally deduct realized CFD losses against future capital gains. Utilizing this deduction provides a critical hedging tool for professionals managing comprehensive, multi-asset portfolios.

3.2. Legal Accessibility and ESMA Restrictions

Regulatory bodies govern these instruments with different levels of scrutiny, restricting global accessibility. Within the EU, the European Securities and Markets Authority (ESMA) enforces strict boundaries to protect retail capital (ESMA, 2018). ESMA mandates impose leverage limits, capping major forex pairs at 30:1 and equities at 5:1, while enforcing negative balance protection, a standard also monitored by the FCA in the UK (FCA, 2024).

Global availability diverges sharply. While CFDs are popular in Europe and Australia, the SEC prohibits their distribution in the United States due to their over-the-counter nature (Investopedia, 2024). Spread betting remains ring-fenced within the UK and Ireland due to its specific regulatory classification overseen by the FCA.

4. Order Execution and Risk Management Strategies

Navigating highly leveraged derivative markets demands strict operational discipline. Implementing automated execution orders remains the only proven method to protect trading capital from sudden macroeconomic volatility.

4.1. CFD Margin Allocation and Protective Orders

Managing a CFD portfolio requires practitioners to constantly monitor utilized margin and available equity. Deploying capital efficiently means calculating exact leverage constraints before executing any trade.

Adhering to ESMA and FCA leverage restrictions remains mandatory for all regulated brokerages operating within the European Economic Area (ESMA, 2018; FCA, 2024). Operating under a 5:1 ESMA-compliant leverage limit on a $1,000 equity position, for instance, strictly dictates a $200 initial margin requirement.

Securing profits and truncating losses relies on mastering specific operational commands:

- Stop-Loss Orders: Liquidating a depreciating position automatically when the underlying asset breaches a pre-defined technical invalidation level. Mastering how to calculate stop loss effectively is a critical skill for maintaining capital longevity in high-leverage environments.

- Take-Profit (Limit) Orders: Capturing upside momentum by executing a total position closure exactly at a predetermined target zone.

- Stop Entry Orders: Triggering a new long or short position only after the market confirms a breakout through a specific resistance or support ceiling.

Practical Execution (CFD Risk Metrics):

Anticipating a bullish breakout on an asset currently trading at $100, a practitioner places a Buy Stop order at $102. Protecting the allocated capital involves setting a strict Stop-Loss at $98 (risking $4 per share). Simultaneously, the operator places a Take-Profit Limit at $110, locking in a mathematically sound 1:2 risk-to-reward ratio.

4.2. Spread Betting Stake Sizing and Gap Risk Mitigation

Structuring spread betting exposure relies entirely on calculating the point-distance to the technical invalidation level, rather than tracking percentage drawdowns. Controlling position sizing means adjusting the stake-per-point precisely to match a predetermined maximum loss threshold.

Mitigating catastrophic market gap-risk (such as weekend price jumps) requires utilizing specialized tools unique to these betting platforms:

- Guaranteed Stop-Loss Orders (GSLO): Paying a fractional premium guarantees the brokerage will execute the stop-loss at the exact requested price, completely eliminating negative slippage during extreme market crashes.

- Trailing Stops: Locking in floating profits automatically by instructing the stop-loss order to trail the active market price at a defined point-distance as the trend matures.

Practical Execution (Spread Betting Sizing):

Initiating a long position on the UK100 at 7500, an operator decides the absolute maximum acceptable portfolio risk is £200. Identifying major technical support at 7460 (a 40-point drop), the trader calculates the exact exposure: dividing the £200 risk by 40 points establishes a strict £5 stake per point. Placing a Guaranteed Stop-Loss at 7460 ensures the maximum drawdown remains hard-capped at £200, regardless of sudden liquidity flashes.

5. Applied Trading Strategies for Each Instrument

Aligning the correct derivative structure with a specific market approach separates professional practitioners from retail novices. Selecting between CFDs and spread betting largely depends on the chosen timeframe and structural market conditions.

5.1. CFD Strategy: Trend-Following and Position Scaling

Executing CFDs aligns perfectly with macro trend-following systems. Capturing prolonged market moves requires identifying an established directional bias and deploying capital with strict risk-to-reward geometry. The contract-based nature of CFDs allows for highly precise volume manipulation during a live trade.

Professional operators frequently utilize a scaling-in approach, adding fractional contract volume to winning positions as the trend confirms itself through consecutive higher highs or lower lows. Conversely, scaling out involves liquidating partial contract blocks at predetermined profit targets. Executing this partial closure secures realized gains while letting the remainder of the position capture maximum upside potential, a key tactic within broader CFD trading strategies.

5.2. Spread Betting Strategy: Range Bound and Momentum Plays

Capitalizing on the tax-free structure of spread betting makes it an ideal vehicle for high-frequency, short-term tactical plays where capturing small, rapid point movements is the primary objective.

- Range Trading: Operators identify consolidated market phases moving sideways. Executing this strategy involves placing long wagers directly near established support floors and initiating short wagers near structural resistance ceilings.

- News-Based Momentum: Deploying momentum strategies during high-impact macroeconomic data releases (such as Non-Farm Payrolls or central bank rate decisions) allows practitioners to capture explosive price adjustments. Utilizing tight guaranteed stop-losses (GSLOs) during these highly volatile events protects the defined stake-per-point while maximizing the upside of tax-free, rapid point accumulation.

6. Example Trades for CFDs and Spread Betting

Bridging the gap between theoretical mechanics and live execution requires analyzing practical market scenarios. Reviewing these comparative case studies highlights exactly how practitioners deploy these instruments strategically.

6.1. CFD Execution Strategy: Apple (AAPL) Equities

Executing a CFD trade on a major global equity demonstrates the direct, volume-based contract structure. Consider an operator analyzing Apple (AAPL) and anticipating a bullish breakout from a consolidation zone.

- The Action: The trader purchases exactly 1 AAPL CFD contract at an underlying market price of $150.

- The Profit Scenario: Bullish momentum pushes the asset to $155. Closing the position captures a $5 price difference per contract. Multiplying the $5 gain by the single contract generates exactly a $5 gross profit (excluding overnight fees).

- The Loss Scenario: Conversely, a sudden market rejection driving the price down to $145 forces a stop-loss execution, resulting in a strict $5 realized loss.

- Strategy Application: Trading single-unit CFDs allows retail practitioners to gain exact fractional exposure to high-priced equities without committing massive capital. Executing short CFDs against a long physical stock portfolio also provides an ideal, highly accurate hedging strategy during short-term market downturns.

6.2. Spread Betting Strategy: Gold Volatility

Deploying capital on precious metals via spread betting highlights the fixed-risk-per-point framework. Assume a UK-based trader identifies a high-probability macroeconomic catalyst affecting Gold prices.

- The Action: The practitioner establishes a long position, wagering exactly £10 per point of movement at an entry price of $2000.

- The Profit Scenario: Gold rallies strongly to $2015, representing a 15-point positive excursion. Multiplying the 15 points by the £10 stake yields a £150 completely tax-free profit.

- The Loss Scenario: Experiencing a false breakout that drops the asset to $1990 creates a 10-point negative move. Multiplying the 10 points by the £10 stake generates a defined £100 loss directly debited from the account.

- Strategy Application: Trading highly volatile commodities through spread betting allows UK operators to aggressively capture massive intraday price swings. Bypassing capital gains tax obligations entirely transforms short-term scalping or day trading into a mathematically superior strategy compared to traditional taxable vehicles.

7. Pros and Cons of CFDs vs. Spread Betting

Choosing between these two products requires understanding their unique advantages and disadvantages. Here’s a clear breakdown to help you decide.

7.1. Pros and Cons of CFDs

Contracts for Difference remain the industry standard for operators seeking direct exposure to global equity markets and institutional-grade execution environments.

Pros of CFDs:

- Direct Short-Selling Capabilities: Executing CFDs facilitates seamless shorting (selling high to buy back low), allowing operators to capture returns during aggressive market downturns. This mechanism serves as a professional-grade hedging tool, enabling investors to protect their physical stock portfolios from short-term depreciation without liquidating their core holdings.

- Institutional Margin Efficiency: Utilizing CFDs grants magnified market exposure through high-tier leverage. For instance, maintaining a $5,000 position in a major equity index typically requires only a $1,000 margin deposit (at 5:1 leverage). This capital efficiency allows traders to diversify across multiple global asset classes simultaneously with a relatively small starting balance.

- Direct Market Access (DMA) and Tight Spreads: Operating with DMA-enabled CFD accounts provides transparency into the exchange’s order book. Practitioners benefit from raw market spreads, ensuring that high-volume orders, such as scalping 100 shares of Apple (AAPL), are executed with minimal slippage and maximum price precision.

- Strategic Tax-Loss Offsetting: Generating realized losses on CFD positions provides a unique fiscal advantage. Practitioners can legally utilize these losses to offset future Capital Gains Tax (CGT) liabilities across their broader investment portfolio—a structural hedging tool entirely absent in spread betting.

Cons of CFDs:

- Compounding Overnight Swaps: Maintaining leveraged CFD positions beyond the daily market close incurs financing fees (swaps). For long-term swing traders, these daily interest charges can progressively erode net profitability.

- Strict Regulatory Reporting: Unlike the tax-free simplicity of betting, every closed CFD trade constitutes a taxable event. Practitioners must maintain meticulous records of entry prices, exit prices, and timestamps to comply with standard Revenue & Customs reporting requirements.

7.2. Pros and Cons of Spread Betting

Evaluating this specialized derivative reveals distinct structural advantages tailored specifically for highly tactical, precise market participation.

Pros of Spread Betting:

- Tax-Free Capital Accumulation: Securing profits through spread betting remains completely exempt from UK Capital Gains Tax (CGT) and stamp duty. Bypassing these fiscal obligations dramatically accelerates long-term account compounding.

- Granular Risk Control: Structuring trades using a ‘stake-per-point’ metric grants operators microscopic control over position sizing. Wagering amounts as small as 50 pence or £1 per point allows practitioners to meticulously manage drawdowns, providing a massive risk-management advantage during volatile news events.

- Lower Absolute Margin Thresholds: Deploying capital via spread betting provides unparalleled accessibility for smaller retail portfolios. While regulatory leverage ratios remain strictly identical to CFDs, the ability to execute micro-stakes means operators can enter global markets without funding the larger initial margin deposits typically required for standard CFD contract lots.

Cons of Spread Betting:

- Geographical Restrictions: Operating these tax-advantaged accounts remains strictly ring-fenced to residents of the UK and Ireland, severely limiting global accessibility.

- Wider Execution Spreads: Brokerages internalize the cost of zero-commission trading by slightly widening the bid-ask spread compared to direct market access (DMA) CFD equivalents.

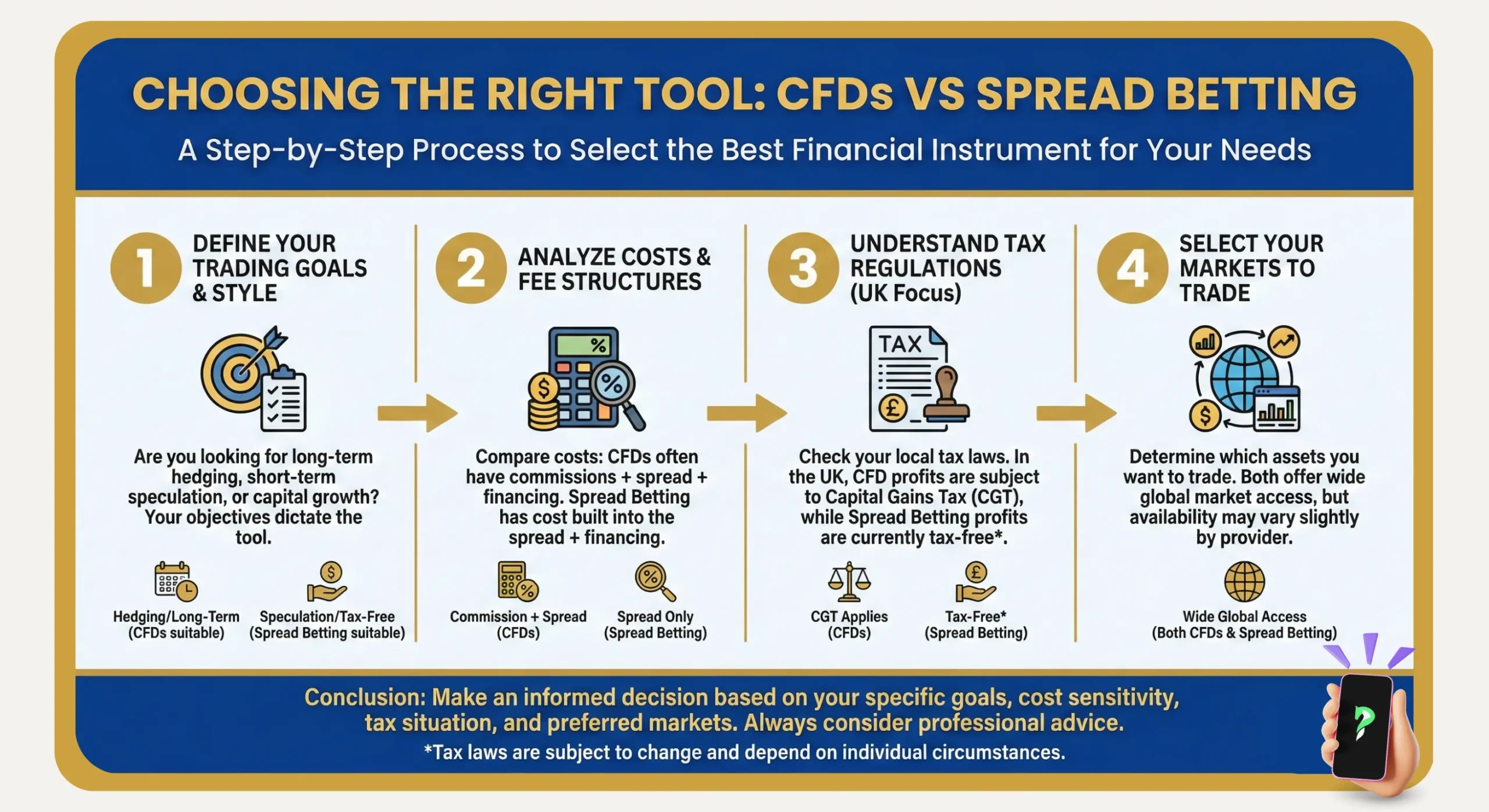

8. Which Is Better for Traders?

There is no single “best” choice; the right answer depends on your circumstances. The decision primarily comes down to your location, tax situation, preferred trading style, and the profit potential you are aiming for.

For UK & Ireland traders

For traders residing in the UK and Ireland, spread betting often has a significant advantage due to its tax treatment. Because profits are typically exempt from capital gains tax, it can be a more efficient way to build capital.

For global traders

For traders outside of the UK and Ireland, the choice is simple: CFD is the go-to instrument. They are globally recognized, widely regulated, and offer deep liquidity. Spread betting is generally not available in most other parts of the world.

Depending on trading style

- Day traders & scalpers: Many high-frequency traders in the UK prefer spread betting because of its simplicity and tax-free status.

- Long-term investors & hedgers: Traders with longer time horizons might prefer CFD. The ability to offset losses against future profits can be a valuable strategic tool.

9. Frequently asked questions about CFDs vs Spread Betting

10. Summary

Both CFDs vs spread betting are powerful instruments for traders. The choice is not about which is universally “better,” but which is right for you.

For traders in the UK and Ireland, the tax advantages of spread betting make it a highly compelling option. For global traders, the worldwide market access, flexibility, and ability to use them for hedging make CFDs the more versatile choice.

Now that you understand the key differences, the next step is to master the strategies themselves. We encourage you to continue your learning journey by exploring our comprehensive guides in the Trading Strategies category on Piprider.

Infographic Section

-

CFDs vs. Spread Betting: A Comparative Guide -

Choosing the right tool: CFDs vs. Spread Betting -

Strategies for CFDs & Spread Betting: A Trading Mind Map