If you are looking for how to find the required reserve ratio (RRR), the most direct way is to check the official monetary policy publications of a country’s central bank. The RRR is a set percentage that dictates how much of a bank’s total deposits must be held in reserve and cannot be loaned out.

Piprider will show you exactly where to find these official central bank rates, explain the reserve requirement formula to calculate the exact dollar amount a bank must hold, and show how this tool impacts the broader economy.

Key Takeaways

- The Required Reserve Ratio (RRR), or reserve requirement, is the percentage of deposits a bank must hold in reserve, set by the central bank.

- To find the official RRR, you must check the central bank’s reserve requirement policy (like the Fed or ECB).

- The Formula: The equation (Required Reserves / Total Deposits) is used to calculate the required dollar amount (given the RRR) or to analyze a specific commercial bank’s actual reserve position.

- It is a monetary policy tool used to manage the money supply, control inflation, and ensure bank liquidity.

- The RRR directly impacts the “money multiplier”; a lower ratio allows banks to lend more, increasing the money supply.

- The US Federal Reserve (Fed) set the RRR to 0% in March 2020, but other major central banks (like the ECB and PBoC) still use it as a policy tool.

1. What Is the Required Reserve Ratio?

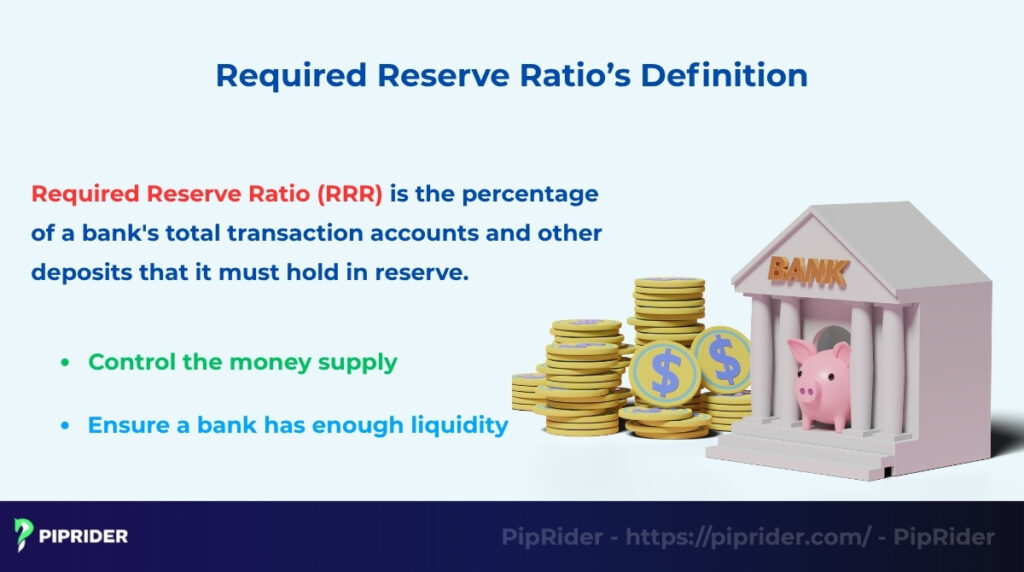

The Required Reserve Ratio (RRR or cash reserve ratio) is the percentage of a bank’s total transaction accounts and other deposits that it must hold in reserve, meaning it cannot be loaned out. It is a key monetary policy tool set by a country’s central bank (like the U.S. Federal Reserve).

The RRR has two main goals. First, it helps ensure a bank has enough liquidity to meet customer withdrawals and prevent a run on a bank. Second, the central bank uses it to control the money supply in the economy.

For example, if the RRR is 10%, a bank must hold $10 in reserve for every $100 of customer deposits. The bank can only lend out the remaining $90.

2. Why Does the Required Reserve Ratio Matter?

The reserve requirement matters because it is a powerful monetary policy tool that central banks use to directly influence a country’s money supply and credit availability. Along with Open Market Operations (OMO) and the Discount Rate, the RRR is one of the three classic tools of macroeconomic policy.

Its most direct impact is on bank lending capacity:

- Increasing the RRR: When the central bank raises the ratio, banks must hold more money in reserve. This reduces their ability to lend and tightens their lending practices, which slows down the money supply and helps control inflation.

- Decreasing the RRR: When the central bank lowers the ratio, banks have more excess reserves. This increases their ability to lend, which expands credit, boosts the money supply, and helps stimulate economic growth.

By changing this single metric, a central bank can influence interest rates, inflation, and the overall pace of the economy.

2.1. Why the RRR Matters for Forex Traders

For forex traders, the Required Reserve Ratio is a vital leading indicator for currency valuation. When a central bank changes the RRR, it immediately alters domestic liquidity and credit conditions, directly impacting exchange rates:

- Expansionary Policy (RRR Cuts): Lowering the ratio injects capital into the banking system, fostering a “risk-on” environment. This influx of liquidity often weakens the domestic currency but can drive capital toward high-yielding Emerging Market (EM) currencies and fuel carry trades.

- Contractionary Policy (RRR Hikes): Raising the ratio tightens credit, triggering “risk-off” sentiment. This typically strengthens the domestic currency as capital becomes scarce and interest rates indirectly rise.

By monitoring these adjustments, traders can spot critical policy clues before bear markets and position themselves ahead of massive sentiment shifts after policy moves.

3. How to Find the Required Reserve Ratio: The Formula

While the central bank publicizes the official percentage, students and financial analysts use the reserve requirement formula for two practical reasons: to calculate the exact dollar amount a bank is forced to hold, or to reverse-engineer a bank’s effective reserve ratio based on its balance sheet.

3.1. Basic Formula

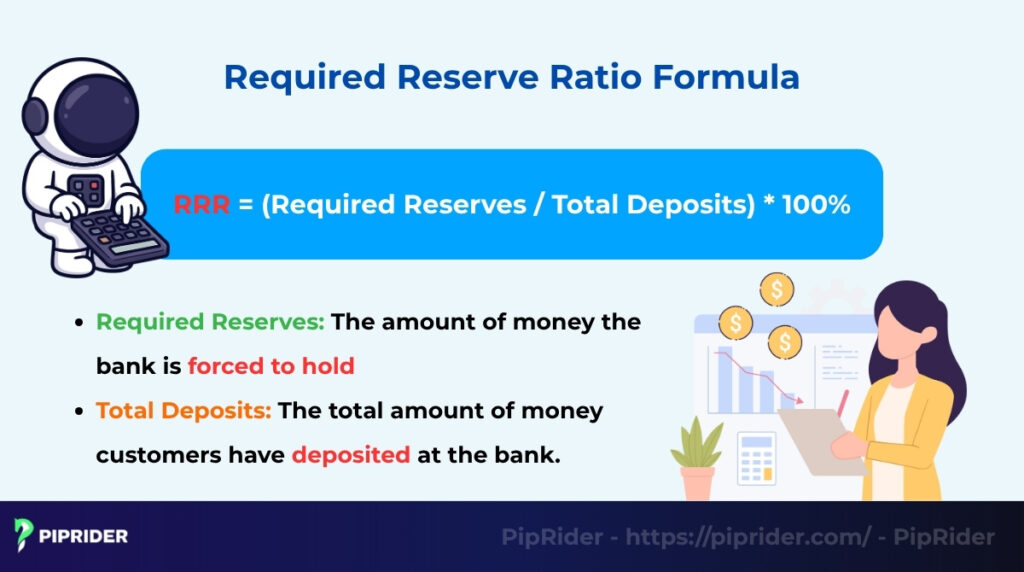

The formula to find the Required Reserve Ratio (RRR) is:

Required Reserve Ratio (RRR) = (Required Reserves / Total Deposits) × 100%

- Required Reserves: The amount of money the bank is forced to hold.

- Total Deposits: The total amount of money customers have deposited at the bank.

3.2. Example Calculation

Let’s use an example to see how to find the required reserve ratio:

- A bank has $200 million in total customer deposits.

- The central bank requires it to hold $20 million in reserves.

- Formula: RRR = ($20,000,000 / $200,000,000) × 100%

- Result: The Required Reserve Ratio = 10%

3.3. Finding Required Reserves Given the Ratio

You can also use the formula to find the dollar amount of reserves if you already know the ratio.

Formula:

Required Reserves = RRR × Total Deposits

- Example: The RRR is 12% and a bank has $500 million in deposits.

- Calculation: 0.12 × $500,000,000 = $60 million

- Result: The bank must hold $60 million in required reserves.

4. How to Find the Required Reserve Ratio in Real Data

While the formula is simple, how to find required reserve ratio data in the real world involves two parts: finding the official reserve requirement set by the central bank and finding the data from a specific commercial bank’s reports.

4.1. Step 1: Check Central Bank Official Sources (By Region)

To find the exact, current Required Reserve Ratio, you must bypass secondary sources and check the central bank’s official monetary policy publications. Here is what to look for regarding major economies:

- United States (The Fed): The Federal Reserve publishes its reserve requirements under Regulation D. You can track historical changes and the current mandate by searching for the official “Federal Reserve Reserve Requirements” release. (Current status: Reduced to 0% effective March 26, 2020) (Federal Reserve Board, 2020).

- Euro Area (ECB): The European Central Bank details its policy on its official portal. Look for the “ECB minimum reserve requirements” explainer, which outlines their current standard ratio of 1% on specific liabilities (European Central Bank, n.d.).

- China (PBoC): The People’s Bank of China actively uses the RRR as a dynamic tool. To find the latest rates, analysts monitor official “PBoC announcements” or major state media releases, such as the comprehensive 0.5 percentage point RRR cut implemented in early 2025 (People’s Bank of China, 2025).

- Vietnam (SBV): The State Bank of Vietnam updates its operating interest rates and reserve requirement ratios directly on the SBV Official Web Portal under the Monetary Policy framework section.

4.2. Step 2: Identify the Bank’s Required and Actual Reserves

To see how the ratio is applied, an analyst would look at a commercial bank’s financial statements. This data is typically found in the bank’s quarterly or annual report, specifically on the balance sheet.

You would look for line items such as “Cash and Balances with Central Banks” or “Cash and Due from Banks.” This figure represents the bank’s actual reserves. A bank’s report may also state its required reserves separately from its excess reserves (any amount held above the reserve requirement).

4.3. Step 3: Apply the Formula

An analyst or student would then apply the formula to this real data. This is not to “discover” the ratio (which is already set by the central bank) but to verify the bank’s compliance and to analyze its liquidity position.

Formula: RRR = (Required Reserves / Deposits) × 100%

This calculation reveals if the bank is meeting its requirement, how much “excess reserve” (extra cash) it holds, and how much of its deposit base is “locked up” versus being used for lending.

5. The Textbook Relationship: RRR and the Money Multiplier

The Required Reserve Ratio is a powerful tool because it directly determines the “Money Multiplier” (MM). The MM is a concept that shows the maximum amount of new money that can be created in the banking system from an initial deposit. This process of credit creation is the basis of fractional reserve banking.

The formula is:

Money Multiplier (MM) = 1 / Required Reserve Ratio (RRR)

Let’s look at the examples from your outline:

- If RRR = 10% (or 0.10):

- Money Multiplier = 1 / 0.10 = 10

- If RRR = 20% (or 0.20):

- Money Multiplier = 1 / 0.20 = 5

This calculation shows that when the RRR is decreased (from 20% down to 10%), the Money Multiplier increases (from 5 to 10). This allows the banking system to create much more money from the same initial deposit, which expands the total money supply.

Important Note on Real-World Application: While the 1/RRR formula is a foundational textbook concept, it is a highly simplified model. In the real-world modern banking system, actual money creation does not expand to infinity. It is heavily constrained by a bank’s willingness to lend, consumer demand for credit, the amount of excess reserves banks choose to hold, and other strict regulatory frameworks like the Liquidity Coverage Ratio (LCR).

6. Real-World Examples: The Fed vs. PBoC

Central banks use the reserve requirement very differently depending on their economic goals. The United States and China provide a clear contrast.

6.1. The U.S. Federal Reserve (Fed)

Before 2020, the U.S. Federal Reserve used a tiered system, where the RRR could be anywhere from 0% to 10% depending on the size of the bank’s transaction accounts.

However, in response to the COVID-19 pandemic, the Federal Reserve took the historic step of eliminating this mandate. The Fed officially reduced reserve requirement ratios to zero percent effective March 26, 2020 (Federal Reserve Board, 2020). This action was taken to ensure banks had maximum liquidity to lend to households and businesses during the crisis.

6.2. The People’s Bank of China (PBoC)

In contrast, the People’s Bank of China (PBoC) still actively uses the RRR as a primary monetary policy tool. Rather than a single universal number, the required ratio varies significantly depending on the size and type of the financial institution. The PBoC actively adjusts these rates to manage economic growth; for example, implementing a 0.5 percentage point cut across the board in early 2025 to inject long-term liquidity into the banking system (People’s Bank of China, 2025).

7. What Are Common Mistakes and Misunderstandings?

While the concept seems simple, several common misunderstandings can confuse students and analysts. The most frequent errors involve confusing the RRR with capital requirements, assuming the ratio is a fixed, universal number, and not understanding its indirect effects.

- Confusing RRR with capital requirements: These are not the same. The RRR is the percent of deposits from depositors a bank must hold. Capital requirements (like those in Basel III) are the amount of its own money (equity) a bank must have to absorb potential losses.

- Assuming the RRR is fixed: The ratio is not a universal constant. It changes by country and over time based on local economic conditions. As noted, the U.S. ratio is currently 0%, while other countries’ ratios are much higher.

- Missing the interest rate connection: Many don’t realize that the RRR indirectly affects interbank interest rates. When the RRR is high, banks have less “excess” cash, so they must borrow more from each other, which can push interbank lending rates higher.

8. Frequently Asked Questions (FAQ)

9. Conclusion

The Required Reserve Ratio is a key tool in monetary policy that helps maintain economic stability. Knowing how to find required reserve ratio and understanding its impact gives us a deeper insight into fractional reserve banking and the mechanisms of monetary control. Even though the RRR for transaction accounts is no longer a primary tool in some countries, the concept remains a fundamental part of every economics and finance education.

To learn more about how economic policy impacts the markets, explore the full library of guides at Piprider.com.