Your home is often your most valuable asset, but its value is “locked in.” If you need a large amount of capital for a major expense, like a home renovation, debt consolidation, or education costs, home equity lending is a common way to access those funds. A home equity loan allows you to borrow against the value you have built up in your property.

However, this also means you are using your house as security, which carries significant risk. This guide will explain exactly what a Home Equity Loan (HEL) is, how it’s calculated, and how it compares to its flexible alternative, so you can make an informed decision.

Key Takeaways

- Lump-Sum Loan: Provides cash in a single, upfront payment.

- Fixed Rate & Payments: Offers a fixed interest rate with predictable monthly payments.

- Uses your home equity as collateral, which means lower rates but carries the risk of foreclosure.

- The loan amount is based on your home’s equity, calculated via a Combined Loan-to-Value (CLTV) ratio.

- A HEL is a fixed-rate lump sum, while a HELOC is a variable-rate credit line.

- Best for large, one-time expenses (like a renovation) where you want a stable repayment schedule.

1. What Is a Home Equity Loan?

A home equity loan (HEL) is a type of loan that allows a homeowner to borrow money using their home’s equity as collateral. Equity is the portion of the home the owner truly “owns” (the market value minus the mortgage balance).

A home equity loan provides the borrower with a single, lump-sum payment upfront. The loan is then repaid over a fixed term, typically 5 to 30 years, with predictable monthly payments at a fixed interest rate. Because this home equity loan is taken out against the home’s value, separate from the primary mortgage, it is often called a “second mortgage.”

According to data from ICE Mortgage Technology (2024), American homeowners are currently sitting on a record $11.5 trillion in tappable equity. This immense wealth represents a primary source of capital for financing major life goals.

Furthermore, TransUnion’s 2025 analysis highlights that the average mortgage holder now possesses over $200,000 in available equity, driving a resurgence in home equity lending. Such borrowing provides homeowners with access to significant funds at interest rates often far below those of traditional consumer credit or personal loans.

2. How a Home Equity Loan Works

A home equity loan functions in a few clear, distinct steps, from calculating your equity to receiving your funds and repaying the loan.

2.1. Determining Your Home Equity

First, the lender must determine how much equity you have. Equity is the difference between what your home is worth and what you still owe on it.

The Formula:

Home Equity = Your Home’s Current Market Value – Your Mortgage Balance

A Simple Example: If your home is valued at $400,000 and you still owe $250,000 on your primary mortgage, you have $150,000 in home equity.

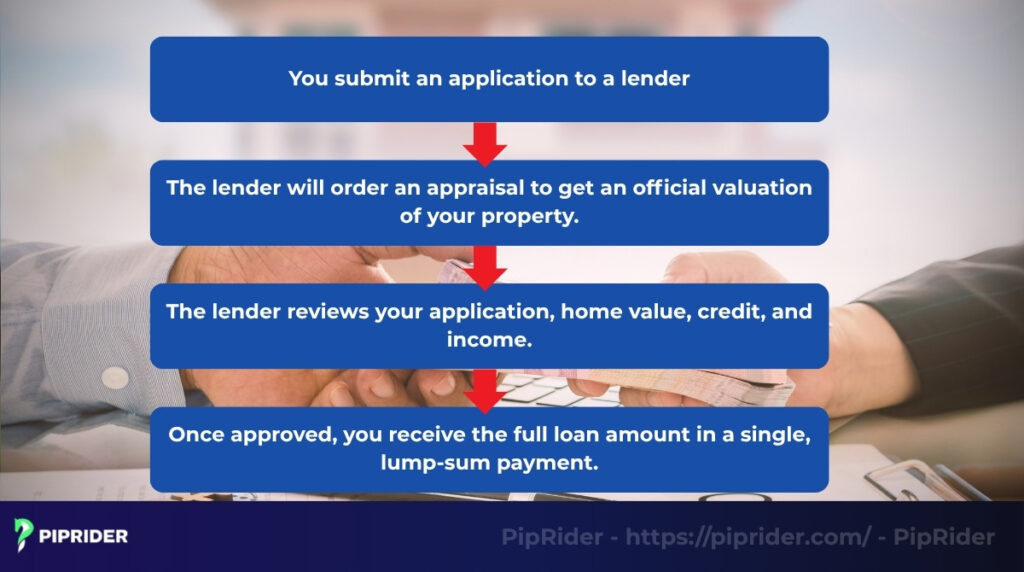

2.2. The Step-by-Step Loan Process

The process for obtaining a home equity loan is similar to getting a regular mortgage:

- Apply: You submit an application to a lender (bank, credit union).

- Appraisal: The lender will order an appraisal to get an official valuation of your property.

- Approval: The lender reviews your application, home value, credit, and income.

- Receive Funds: Once approved, you receive the full loan amount in a single, lump-sum payment.

After receiving the money, you begin repaying the loan in fixed monthly installments, which include both principal and interest, at a fixed interest rate.

2.3. Interest and Repayment

The repayment structure is one of the main features of this second mortgage.

- Fixed Interest Rate: The interest rate is locked in at the beginning and will not change for the entire life of the loan. Fixed interest rates make budgeting predictable, as you always know exactly what your payment will be.

- Stable Payments: Your monthly payment remains the same every month for the full repayment term of the loan (e.g., 5, 15, or 30 years).

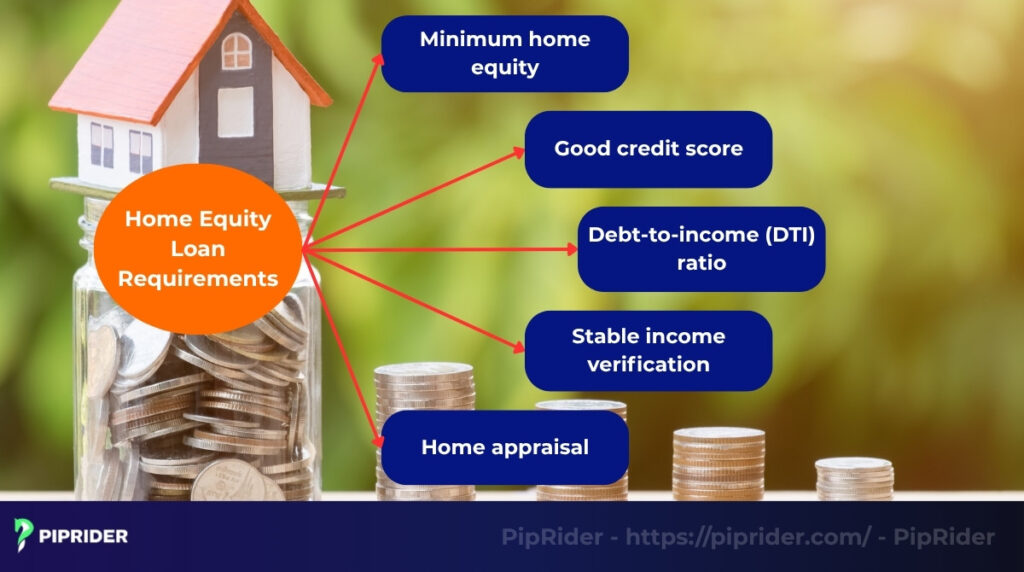

3. Home Equity Loan Requirements: Key Eligibility Benchmarks

Lenders establish specific financial thresholds to ensure borrowers can sustain a second mortgage. Meeting these requirements is essential for approval and for securing the most competitive interest rates.

3.1. Credit Score Standards

Credit health is a primary factor in the approval process. According to Experian, while some lenders may accept a FICO score as low as 620, a score of 680 or higher is typically required to access favorable terms. A higher credit score not only improves the likelihood of approval but also directly reduces the long-term cost of the loan through lower interest rates.

3.2. Debt-to-Income (DTI) Ratio

The Debt-to-Income (DTI) ratio measures a borrower’s ability to manage monthly payments. LendingTree emphasizes that most financial institutions prefer a DTI of 43% or less. Such a limit ensures that the homeowner has sufficient cash flow to cover existing debts alongside the new home equity loan payments.

3.3. Combined Loan-to-Value (CLTV) and Equity Stake

Maximum borrowing limits depend on the property’s current appraised value and the lender’s specific CLTV threshold. Experian reports that most financial institutions cap the Combined Loan-to-Value (CLTV) ratio at 80% to 85%. A mandatory 15% to 20% equity buffer serves as a critical safeguard against market volatility, preventing homeowners from falling “underwater” if property values decline during a market correction.

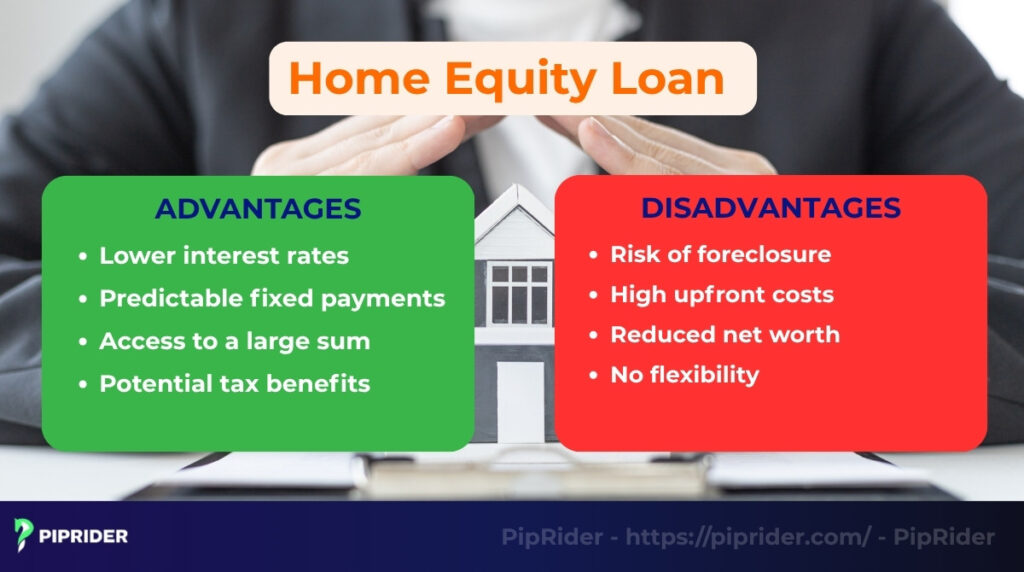

4. Advantages and Disadvantages

A home equity loan can be a useful financial tool, but it is important to understand both the benefits and the significant risks involved.

4.1. Advantages

A home equity loan offers several clear benefits compared to other types of debt.

- Lower interest rates: Because the home equity loan is secured by your home, lenders offer much lower interest rates than you would get with unsecured consumer debt like personal loans or credit cards.

- Predictable fixed payments: The interest rate is fixed for the life of the loan. This means the monthly payment never changes, which makes budgeting simple and predictable.

- Access to a large sum: Homeowners can often borrow a significant amount of money (typically up to 80-85% of their equity), which is ideal for large, one-time projects.

- Potential tax benefits: In the U.S., the interest paid on a home equity loan may be tax deductible. However, the rules changed with the Tax Cuts and Jobs Act of 2017 (which superseded rules from the Tax Reform Act of 1986). Interest is now only tax deductible if the funds are used to “buy, build, or substantially improve” the home that secures the loan (according to IRS rules) (Internal Revenue Service [IRS], 2024; Congress.gov, n.d.).

4.2. Disadvantages

The risks of an equity loan are significant and must be taken seriously.

- Risk of foreclosure: The risk of foreclosure is the most significant drawback. Because the loan is a second mortgage secured by your house, you could lose your home if you fail to make the monthly payments.

- High upfront costs: These loans often come with closing costs, just like a primary mortgage. These can include appraisal fees, origination fees, and title fees, which can add up.

- Reduced net worth: You are borrowing against the value you have built in your home. This process reduces your home equity and increases your total debt.

- No flexibility: You receive the money in one lump sum. Unlike a HELOC (Home Equity Line of Credit), you cannot draw more money as you pay the loan down. It is a one-time transaction.

Maintaining an emergency fund in high-yield savings can help ensure you stay current on payments during unexpected financial difficulties, reducing your foreclosure risk.

5. Home Equity Loans vs. HELOCs: A Technical Comparison

Choosing between a home equity loan (HEL) and a home equity line of credit (HELOC) is a pivotal financial decision. While both options leverage a second mortgage structure, their disbursement methods and interest profiles differ fundamentally.

Market Rates Snapshot (Updated: February 2026)

HELOC rates are typically variable and adjust according to the U.S. Prime Rate plus a lender’s specific margin. Data from Bankrate indicates that the national average HELOC rate stands at approximately 7.31% (as of Feb 4, 2026).

Note: Interest rates fluctuate daily based on broader market conditions, regional competition, and individual credit profiles. Borrowers should request a personalized quote for the most accurate terms.

5.1. Feature Comparison Table

The following table outlines the structural differences between these two equity-based products to help you identify the best fit for your cash flow needs.

| Feature | Home Equity Loan (HEL) | Home Equity Line of Credit (HELOC) |

|---|---|---|

| Disbursement | A single, upfront lump-sum payment. | A revolving credit line that can be drawn from as needed. |

| Loan Phases | Single Phase: Repayment of principal and interest begins immediately. | Two Phases: A “Draw Period” (typically 10 years) followed by a “Repayment Period” (typically 20 years). |

| Interest Rate | Fixed: Locked for the entire life of the loan, protecting against market hikes. | Variable: Adjusts based on the Prime Rate; subject to market volatility. |

| Repayment Type | Fully Amortized: Level monthly payments from start to finish. | Interest-Only Options: Often available during the draw period, leading to larger payments later. |

| Primary Risk | Equity Erosion: Reduces your home’s net worth immediately upon funding. | Payment Shock: Monthly obligations can spike significantly when the draw period ends. |

5.2. Critical Considerations: Draw Periods and Payment Shock

The dual-phase structure of a HELOC requires disciplined financial planning. During the initial 10-year draw period, many borrowers opt for interest-only payments to keep costs low. Such a strategy often leads to a significant payment shock once the 20-year repayment phase begins, as principal payments suddenly become mandatory alongside variable interest.

In contrast, a home equity loan provides the safety of a fixed interest rate. Predictable monthly installments protect the homeowner from rising interest rates, making it an ideal choice for debt consolidation or major home improvements where the budget is strictly defined.

Lenders generally enforce a Combined Loan-to-Value (CLTV) limit of 80% – 85% for both products. Maintaining an equity buffer of at least 15% – 20% remains a standard requirement to mitigate the risk of foreclosure in a declining housing market.

5.3. HELOC Mechanics: The Road to Payment Shock

A Home Equity Line of Credit (HELOC) is often misunderstood as a permanent revolving fund. In reality, the structural transition between its two distinct phases creates a significant financial cliff for unprepared borrowers.

- The Draw Period (Typically 10 Years): During this initial decade, the borrower can withdraw funds up to the credit limit and usually has the option to make interest-only payments. While low monthly obligations during this phase provide a sense of affordability, the principal balance remains untouched. The lack of amortization means the borrower still owes the full original amount after ten years of payments.

- The Repayment Period (Typically 10–20 Years): Once the draw period expires, the line of credit “freezes,” and further withdrawals are prohibited. Borrowers must then repay both principal and interest over the remaining term.

Why “Payment Shock” Occurs

Payment shock describes the sudden, massive increase in monthly obligations when the interest-only phase ends. Such a shift can cause payments to double or even triple, as the borrower must now amortize the full principal over a shorter remaining window (e.g., 20 years).

Because HELOCs feature variable interest rates, a market rate hike occurring simultaneously with the start of the repayment phase creates a “double whammy” effect. This compounding pressure is why experts from Kiplinger and other financial authorities warn that HELOCs require much stricter long-term budgeting than fixed-rate products.

6. Special Considerations

Before taking out a home equity loan, it is crucial to understand the specific terms, costs, and legal rights associated with the loan.

6.1. The Right of Rescission: A Legal Safeguard

Federal law provides a specific safety net for homeowners leveraging their primary residence as collateral. Under the Consumer Financial Protection Bureau (CFPB) Regulation Z (1026.23), borrowers are granted a three-business-day “cooling-off” period after signing the closing documents. During this window, the agreement can be canceled for any reason without financial penalty.

Such a protection applies specifically to second mortgages like home equity loans and HELOCs, though it does not extend to purchase-money mortgages used to buy a home. Exercising this rescission requires providing written notice to the lender before midnight of the third business day.

The mandatory waiting period ensures that funds are not disbursed until the right has expired, allowing the homeowner one final opportunity to evaluate the risks of placing a lien on their property.

6.2. Closing Costs

Closing costs represent a significant upfront expense that borrowers must factor into their long-term financial planning. Data from Experian indicates that these fees typically range from 2% to 5% of the total loan amount.

A standard breakdown of closing expenses for a second mortgage usually includes:

- Appraisal Fees: Costs for a professional valuation to determine the home’s current market price.

- Title Search and Insurance: Fees to ensure the property is free of legal liens or ownership disputes.

- Origination Fees: Administrative charges from the lender for processing and underwriting the loan.

- Government Recording Fees: Minor costs to officially record the new lien on the property.

Accounting for these upfront charges is vital when comparing offers, as some lenders may promote “no-closing-cost” loans. While attractive, such options often result in a higher interest rate over the life of the loan to offset the lender’s initial expenses.

6.3. Tax Deductibility and IRS Regulations

Interest paid on a home equity loan or HELOC may offer significant tax advantages under specific federal guidelines. According to IRS Publication 936, interest remains deductible only when the loan proceeds are used exclusively to “buy, build, or substantially improve” the qualified home that secures the debt.

Eligibility for such a tax break requires the homeowner to itemize deductions on Schedule A of their tax return rather than opting for the standard deduction. Furthermore, interest on funds utilized for personal expenses, including debt consolidation, tuition, or vacations, is strictly non-deductible under current tax laws.

While home equity can fund these needs, diversifying your wealth through low-cost investment vehicles like ETFs may be wiser for long-term financial security. Consulting a qualified tax professional is essential to verify eligibility and ensure compliance with the latest IRS mandates.

7. Alternatives to Home Equity Loans

A home equity loan is not the only mechanism for accessing liquidity. Depending on current market interest rates and existing mortgage terms, other financial instruments may provide a more efficient path to capital. Evaluating these alternatives ensures that homeowners do not unnecessarily risk their property or overpay for debt.

7.1. Common Financial Options

- Cash-Out Refinance: A cash-out refinance replaces the current primary mortgage with a new, larger loan. The borrower receives the difference in cash. The primary advantage is the ability to maintain a single monthly payment, though the transaction requires paying closing costs on the entire new loan balance.

- Personal Loan: These are unsecured loans, meaning the home does not serve as collateral. The lack of security protects the property from foreclosure but results in higher interest rates. Personal loans are ideal for smaller amounts where the high cost of a second mortgage appraisal is not justified.

- Reverse Mortgage: Homeowners aged 62 or older with significant equity may qualify for a reverse mortgage. Such an arrangement allows the bank to pay the homeowner through a lump sum or monthly installments. The debt is only settled when the owner sells the home, moves out, or passes away.

7.2. Decision Matrix: When to Choose Which?

The following table identifies specific financial scenarios to help you determine the most strategic choice for your needs.

| Scenario | Optimal Choice | Strategic Reason |

|---|---|---|

| Current market rates are lower than your original mortgage rate. | Cash-Out Refinance | Replacing the entire debt allows you to lower the primary interest rate while withdrawing cash. |

| You need a small amount (under $15,000) and want to avoid appraisal fees. | Personal Loan | Higher interest rates are offset by the lack of closing costs and the speed of funding. |

| You are over 62 and need to supplement retirement income. | Reverse Mortgage | Converting home equity into steady cash flow removes the burden of monthly principal payments. |

| You have a very low interest rate on your primary mortgage that you want to keep. | Home Equity Loan / HELOC | A second mortgage allows you to access capital without resetting the low rate of your primary debt. |

8. How to Compare Offers: A Strategic Checklist

Not all home equity offers are created equal. A lower monthly payment may hide high upfront fees, while a low “teaser rate” often leads to a massive financial spike later. Using a standardized checklist allows for an accurate side-by-side comparison of the true cost of borrowing.

To effectively evaluate competing offers, homeowners should prioritize these six critical factors:

- APR vs. Interest Rate: Evaluating the total cost including fees.

- Upfront Fees and Closing Costs: Identifying out-of-pocket expenses.

- Prepayment Penalties: Checking for hidden costs of an early exit.

- HELOC Specifics: Analyzing teaser rates, margins, and rate caps.

- Repayment Structure: Verifying if payments are interest-only or amortized.

- Total Cost Estimate: Calculating the aggregate expense over the loan life.

8.1. Evaluating the True Cost: APR and Closing Fees

The Annual Percentage Rate (APR) serves as the primary metric for comparison because it incorporates the base interest rate plus points and origination fees. Beyond the rate, homeowners must scrutinize upfront closing costs, which typically range from 2% – 5% of the loan amount. A transparent fee breakdown, including appraisal and title charges, often reveals that a “low-interest” loan with high fees is actually more expensive than its competitors.

8.2. Analyzing Repayment Flexibility and Penalties

The repayment structure dictates long-term affordability. Borrowers should prioritize a fully amortized schedule, where each payment reduces the principal balance from the start. Additionally, prepayment penalties represent a significant hidden risk. Prioritizing lenders with “zero-penalty” terms ensures financial flexibility, allowing the homeowner to sell or refinance without incurring thousands in unexpected exit costs.

8.3. Scrutinizing HELOC Specifics and Total Aggregate Expense

When evaluating a HELOC, looking beyond initial “teaser” rates is essential. Borrowers must verify the Margin and Rate Caps to prevent future payment shock when market rates rise. Instead of focusing solely on monthly bills, calculating the aggregate expense over the entire term provides the truest measure of value. A side-by-side total cost estimate, including all interest, annual fees, and minimum draw requirements, ensures a second mortgage remains a strategic asset.

9. Frequently asked questions about Home Equity Lending

10. 2026 Market Pulse: Home Equity Rates Snapshot

Interest rates for home equity products are highly sensitive to broader economic shifts and Federal Reserve policies. The following benchmarks represent the current national averages for well-qualified borrowers as of early 2026.

| Product Type | Estimated Average Rate | Standard Term |

|---|---|---|

| Home Equity Loan (Fixed) | 8.25% – 9.15% | 15 Years |

| HELOC (Variable) | 8.50% – 10.25% | 10-Year Draw |

| Cash-Out Refinance | 6.75% – 7.50% | 30 Years |

Financial Disclosure: Rates are subject to daily fluctuations based on market volatility and individual lender criteria. Current data serves as a general benchmark sourced from Bankrate (2026). Actual offers depend on your specific FICO score, CLTV ratio, and debt-to-income profile.

11. The Bottom Line

A home equity loan is a major decision in home equity lending. It can be a reasonable financial choice if you are a homeowner with equity and need a loan against equity with a low, fixed interest rate and predictable payments.

However, it is crucial to remember that the loan is secured by your home. The risk of losing your property is real if you cannot make the payments on time.

Before signing, carefully assess your ability to repay, clarify your purpose for the funds, and decide whether a fixed-rate HEL or a flexible HELOC truly matches your financial needs. To stay updated on how interest rate trends impact your financial decisions, follow the Analysis section at PipRider for more insights.