An Integrated Circuit Card (ICC) is a plastic card embedded with an electronic chip that functions as a miniature computer. You likely know this technology by its more common names: “smart card” or “chip card.”

Unlike older magnetic stripe cards that only store static data, the ICC’s embedded chip includes a processor and memory to securely store and actively process information. This technology is the global standard for security in banking (EMV), telecommunications (SIMs), and identity verification.

This article explains the definition of an ICC, how its components function, and its critical applications in modern finance and security.

Key Takeaways

- An Integrated Circuit Card is a “smart card” with a built-in computer chip for processing and memory.

- Widely known as a “smart card,” “chip card,” or in banking, an “EMV card.”

- To provide high-level security for transactions and data, far superior to magnetic stripes.

- The integrated circuit works by running applications and encrypting data, often requiring a PIN or passcode for authentication.

- This technology is used everywhere, including credit card ic chips (EMV), phone SIM cards, and secure government ID cards.

- The technology follows international standards (like ISO/IEC 7816 and EMV) to ensure global compatibility and security.

1. What Is an Integrated Circuit Card (ICC)?

An Integrated Circuit Card (ICC) is a plastic card embedded with a small microchip that is essentially a tiny computer containing a microprocessor and memory used to securely store and process data.

- Common names: You likely know this technology as a “smart card,” “chip card,” or, in banking, an “EMV card.” The term IC card meaning simply refers to the integrated circuit (the chip).

- Primary Purpose: The chip’s main job is to provide enhanced security. According to EMVCo, the organization that manages global payment standards, this chip technology is far superior to old magnetic stripe cards at preventing fraud like cloning or “skimming.”

- Applications: ICCs are used everywhere, including:

- Banking (credit/debit cards)

- Telecommunications (SIM cards)

- Personal Identification (passports, driver’s licenses, ID cards)

- Healthcare (health insurance cards)

- Official Standards: These circuit cards follow global standards to ensure they work everywhere. The main standards are ISO/IEC 7816 for contact cards (the ones you insert) and ISO/IEC 14443 for contactless cards (the ones you tap).

2. Components and Features of an ICC

An Integrated Circuit Card (ICC) is simple on the outside, but it contains a sophisticated miniature computer. Its components and features work together to store and protect information.

2.1. Physical Components

The embedded chip is a sophisticated piece of hardware. While it appears small, it contains a complete computer architecture comprising several key physical parts:

- Microprocessor (CPU): This is the “brain” of the chip. It runs the card’s operating system, manages memory, and most importantly, performs the cryptographic calculations that keep your data secure.

- Memory: Just like a desktop computer, the chip utilizes different memory types. ROM stores the permanent operating system, RAM is used for temporary processing, and EEPROM (or Flash) securely stores user data like account numbers and digital certificates.

- Contacts / Chip Interface: This is the communication bridge between the chip and the terminal. It appears as the gold contact pad (for physical insertion) or exists as a hidden internal antenna (for contactless transactions).

- Protective Body: The plastic card body (usually PVC or polycarbonate) acts as a housing, shielding the delicate internal circuitry from physical damage, bending, and static electricity.

2.2. Functional Features

The physical components enable several key security features.

- Data Encryption & Authentication: The primary function of the integrated circuit is security. The chip can encrypt data it sends to a terminal, making it unreadable to thieves. It also performs a dynamic authentication process to prove to the terminal that the card is genuine (and not a clone).

- Digital Signature Capability: The microprocessor can use stored cryptographic keys to create a digital signature. This is used to authorize financial transactions (like verifying a PIN) or to prove identity in electronic systems.

- Tamper Resistance: The chip is specifically designed to be tamper-resistant. It is extremely difficult to physically access or copy the data stored within it without destroying the chip. This is its single biggest advantage over magnetic stripe cards.

2.3. Real-World Example: How an EMV Transaction Works

To understand the power of the Integrated Circuit Card, let’s look at a standard chip transaction process (EMV). Unlike a simple magnetic swipe, this involves a secure dialogue between the card and the terminal:

- Connection: The terminal powers the chip and establishes a secure connection.

- Authentication (Challenge-Response): The terminal sends a random number (the challenge) to the card. The card uses its internal private key to sign it and sends back a digital response, proving it is authentic without revealing the key.

- Cryptogram Generation: The chip’s microprocessor generates a unique transaction cryptogram, a one-time digital code specific to that exact purchase.

- Validation: The issuer (bank) receives the cryptogram, verifies it against the EMV rules, and approves the transaction. Because this code changes every time, stolen data cannot be reused.

3. Types of Integrated Circuit Cards

Integrated Circuit Cards (ICCs) are classified based on two primary criteria: their embedded capabilities (processing power) and their communication interface (how they connect to readers).

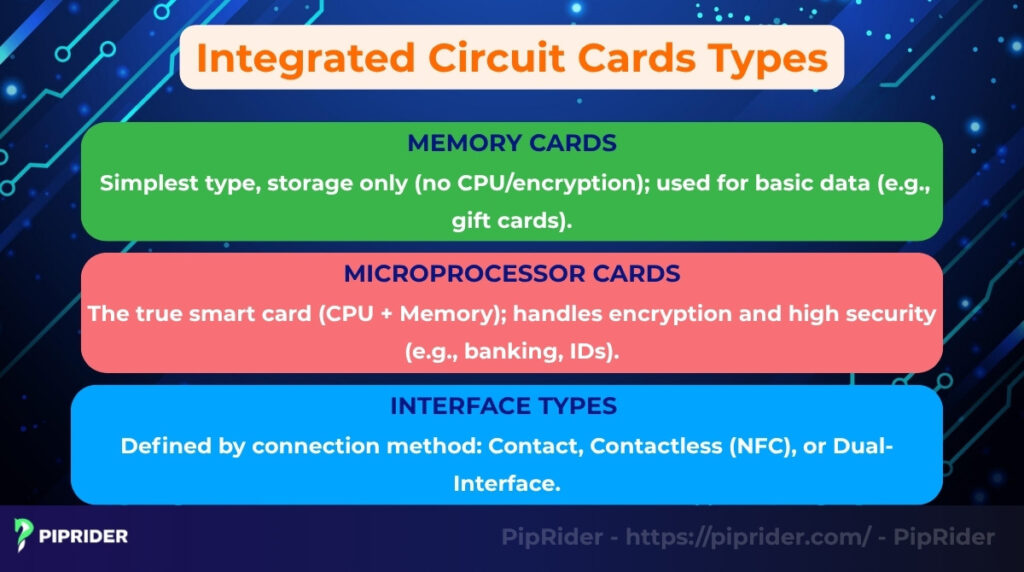

3.1. Memory Cards (Passive Storage)

Memory cards represent the entry-level of ICC technology. They are essentially secure storage devices, functioning similarly to a floppy disk or a simple USB drive, but in a card format. Because they lack complex logic, they are inexpensive to produce.

- Function: They contain only non-volatile memory chips and no microprocessor (CPU).

- Capability: They can store data but cannot process it or execute cryptographic algorithms.

- Use: Best for low-security, cost-sensitive applications like prepaid phone cards, hotel key cards, or simple loyalty cards.

3.2. Microprocessor Cards (Active Processing)

These are what the industry refers to as true “smart cards.” Unlike memory cards, they contain an onboard CPU and an operating system, allowing them to function as miniature, independent computers capable of dynamic interaction.

- Function: They act as intelligent processors capable of executing applications and managing data securely.

- Capability: Their defining feature is active security. They can perform on-chip encryption and mutual authentication to prevent cloning.

- Use: Required for high-security environments, including EMV banking cards, SIM cards, and electronic passports.

3.3. Classification by Interface (Contact vs. Contactless)

Beyond their internal processing capabilities, ICCs are defined by their communication interface, the specific method used to transmit data between the chip and the reader. This classification relies on international standards (ISO/IEC) and determines whether the user must physically insert the card or can simply use wireless technology.

| Type | How It Works | Standards | Common Examples |

|---|---|---|---|

| Contact Card | Requires physical insertion. The reader’s pins must touch the card’s gold contact pad. | ISO/IEC 7816 | Mobile Phone SIM cards Older ATM cards |

| Contactless Card | Uses NFC / RFID technology to communicate via radio waves when “tapped”. | ISO/IEC 14443 | Public transit passes Hotel key cards |

| Dual-Interface Card | Hybrid design containing both interfaces connected to a single chip. | ISO/IEC 7816 & ISO/IEC 14443 |

Modern EMV Credit/Debit Cards Biometric e-Passports |

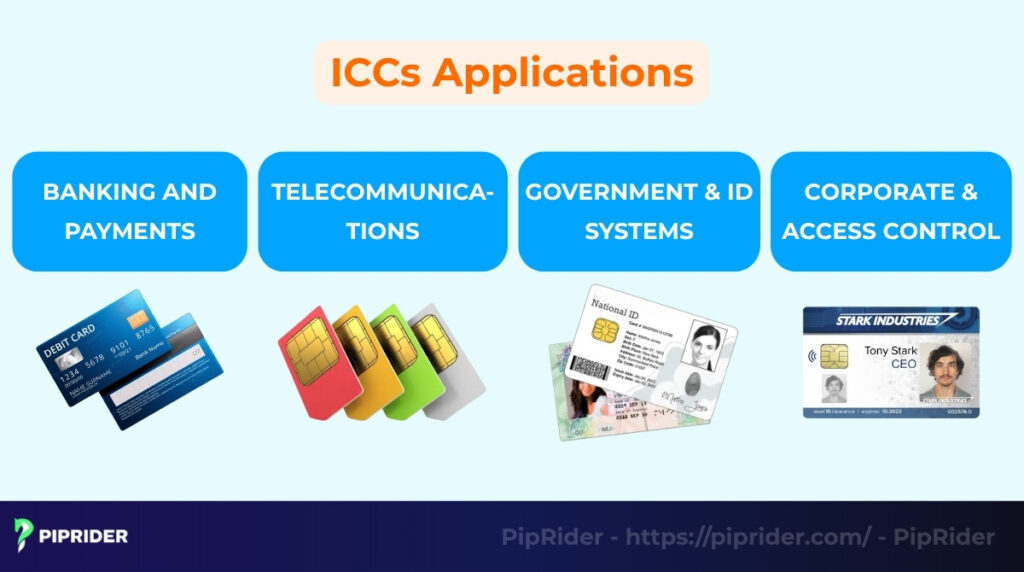

4. Applications in Financial Services and Other Sectors

The technology behind the Integrated Circuit Card (ICC) is used in many areas, but its most important application is in financial services for enhancing security.

4.1. Banking and Payments

This is the most widespread application of ICC technology. The credit card IC chip, technically known as EMV (Europay, Mastercard, Visa), has become the global standard for secure payments, replacing magnetic stripes as the primary authentication method in most major markets.

- Fraud Reduction: The chip’s primary goal is to combat counterfeiting. Unlike magnetic stripes which are easy to copy, the chip is significantly harder to clone, drastically reducing card-present fraud.

- Secure Transactions: During a purchase, the chip actively authenticates the PIN and generates a unique code for that specific transaction, ensuring data cannot be reused if intercepted.

- Note: While the chip is the standard, many cards still retain a magnetic stripe for backward compatibility (fallback) in regions or terminals where chip technology is not yet fully supported.

4.2. Telecommunications

The SIM card (Subscriber Identity Module) in every mobile phone is a small, specialized type of Integrated Circuit Card. Its chip securely stores a unique ID number (IMSI) and authentication keys. This information is used to identify the subscriber to the mobile network, acting as the “gatekeeper” that allows a specific phone to make calls and use data on that network.

4.3. Government & ID Systems

Governments worldwide use ICCs to secure personal data and prevent forgery (U.S. Department of Homeland Security, n.d.). The chip is a highly secure place to store biometric data (like fingerprints or a facial image) and digital certificates. Common examples include:

- National ID cards

- Electronic passports (e-passports)

- Smart driver’s licenses

- Patient ID cards for national healthcare systems

4.4. Corporate & Access Control

Many organizations use ICCs for internal security. The chip on an employee’s ID badge can hold digital credentials. Instead of just a magnetic stripe, the employee must “tap” or “insert” the card into a reader. The reader then communicates with the chip to verify the credential is valid before granting access to a secure building, a specific room, or a company computer network.

5. Security Considerations

The primary driver for the global adoption of the Integrated Circuit Card (ICC) is its superior security architecture compared to legacy magnetic stripes. However, while chip technology significantly raises the barrier for fraudsters, it is important to understand both its strengths and its specific limitations.

5.1. Data Protection Mechanisms

Security on an ICC goes far beyond simple storage. Unlike magnetic stripes, which passively expose static data, the ICC uses an active processor to defend information through two key mechanisms:

- Strong Encryption: The chip’s microprocessor uses robust cryptographic algorithms (such as RSA or ECC) to encrypt data. Even if a criminal intercepts the signal, the data appears as scrambled, unreadable code.

- Mutual Authentication: Before a transaction begins, the card and the terminal perform a secure “handshake” to prove each other’s legitimacy. This prevents criminals from using fake terminals to capture card details.

5.2. Fraud Prevention and Limitations

While the chip is a powerful tool, it is not a magic shield against all types of crime. It is crucial to distinguish between the specific fraud scenarios the chip can effectively stop and those it cannot.

- Combats Counterfeiting (Card-Present): The chip generates a unique transaction cryptogram (a one-time code) for every single purchase. Because this code changes every time, skimmers cannot simply copy the data to create a functioning counterfeit card. This has made physical cloning significantly harder than with magnetic stripes.

- Limitation – Online Fraud (Card-Not-Present): The chip’s physical security features do not automatically prevent fraud online or over the phone. Since the chip is not interacting with a reader during an internet purchase, the “unique cryptogram” is not generated. Therefore, online security must rely on additional layers like CVV codes, Tokenization, and Two-Factor Authentication (2FA).

5.3. Global Standards and Compliance

To ensure that a chip card issued in one country works flawlessly in a terminal in another, ICCs must adhere to rigorous international protocols. These standards guarantee global interoperability.

- ISO/IEC 7816 (For Contact Cards): Managed by the International Organization for Standardization (ISO), this is the foundational standard. It defines the physical dimensions, the gold contact pad location, and the electrical signals used for transmission.

- Official Source: ISO/IEC 7816 Standards (ISO.org)

- ISO/IEC 14443 (For Contactless Cards): This standard governs “proximity” cards used in payments and IDs. It defines the radio frequency (13.56 MHz) and the communication protocol, serving as the basis for modern NFC technology.

- Official Source: ISO/IEC 14443 Standards (ISO.org)

- EMV Specifications (For Application Logic): While ISO defines the “hardware” and communication, EMV (Europay, Mastercard, Visa) defines the “application logic” for secure payments. Managed by EMVCo, these specifications ensure the transaction is encrypted and authenticated correctly on top of the ISO layers.

- Official Source: EMV Specifications (EMVCo.com)

6. Benefits and Limitations of Using ICCs

The global adoption of the Integrated Circuit Card (ICC) has been driven by its clear advantages, but it also comes with specific trade-offs.

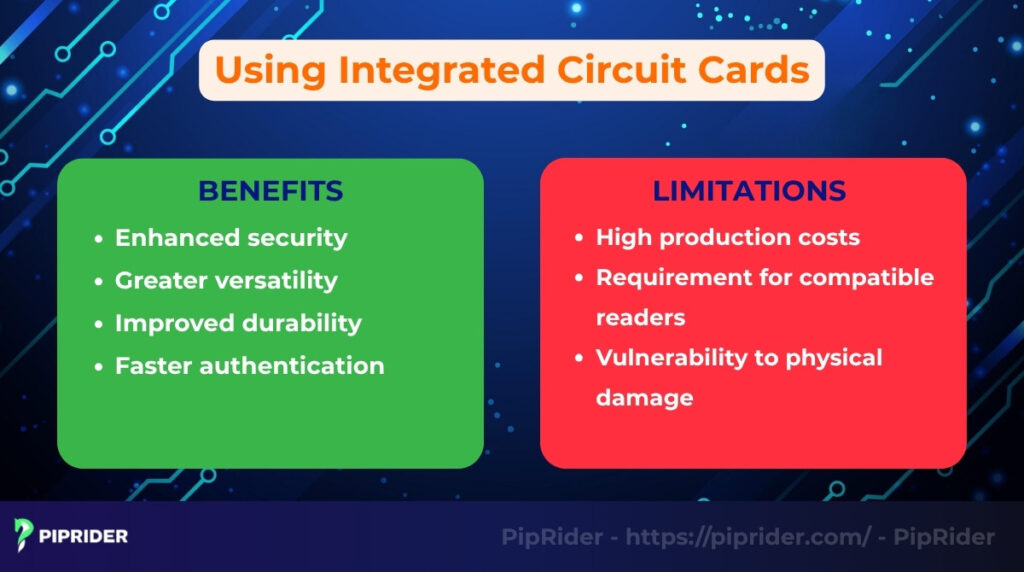

6.1. Benefits

ICCs offer several clear advantages over older magnetic stripe technology:

- Enhanced security: The chip’s microprocessor provides strong data encryption and dynamic authentication. This makes circuit cards extremely difficult to clone (“skim”) or counterfeit, drastically reducing fraud.

- Greater versatility: A single Integrated Circuit Card can securely host multiple applications on one chip, such as a credit application, a debit application, and a building access key.

- Improved durability: The embedded chip is more resilient than a magnetic stripe. It is not easily damaged by magnetic fields and is less prone to “wear and tear” from swiping.

- Faster authentication: With contactless technology (NFC), ICCs allow for much faster authentication. “Tap-to-pay” transactions take a fraction of the time, improving convenience.

6.2. Limitations

Despite their advantages, ICCs also have drawbacks:

- High production costs: The cost to manufacture a smart chip is significantly higher than producing a simple magnetic stripe card, leading to higher issuance costs for banks and other organizations.

- Requirement for compatible readers: To function, ICCs require specialized IC chip readers (either contact or contactless). Upgrading old magnetic-stripe-only terminals (like ATMs and POS systems) is a major expense for merchants and banks.

- Vulnerability to physical damage: While durable, the chip can still be damaged. Bending the card, deep scratches on the contact pad, or exposure to strong static electricity can break the internal card circuit and make the chip unusable.

7. ICCs and Identity Theft Protection

A primary driver for adopting the Integrated Circuit Card (ICC) is its powerful role in preventing identity theft.

7.1. How ICCs Reduce Theft

The chip is an active defense system, unlike the passive magnetic stripe. It protects information in two main ways:

- Encrypted Storage: Personal data stored on the chip is encrypted. Even if a thief could physically access the chip’s data, it would be unreadable without the correct cryptographic keys.

- Mutual Authentication: When you use your card, the card reader and the chip perform a secure “handshake.” They prove to each other that they are legitimate. This stops criminals from using fake terminals to “skim” or steal your card data.

7.2. Comparison to Magnetic Stripe Cards

The difference in security is massive:

- Magnetic Stripe: This is like a nametag with your information written on it for anyone to read. The data is unencrypted and static (it never changes). It is very easy for criminals to copy (“skim”) this data onto a blank card and create a clone.

- ICC (Chip): This is like a secure digital vault. The data is encrypted, and the chip cannot be easily cloned. Each transaction creates a unique, one-time-use code. This makes stolen data from a single transaction useless for creating a fake card.

7.3. Applications in Digital Identity

This high level of security is why ICCs are the standard for digital identity and e-government security. When you use an e-passport or a national smart ID card, the chip securely stores your personal and biometric data. This verifies that you are who you say you are and prevents the creation of fake identities.

8. Future Trends of Integrated Circuit Cards

The technology of the Integrated Circuit Card is rapidly evolving beyond the traditional plastic form factor. The industry is shifting toward biometric integration and complete digitization.

- Biometric Payment Cards: The next generation of ICCs integrates a fingerprint sensor directly onto the card body. This eliminates the need for PINs and raises the spending limit, as the card will not authorize a payment without a biometric match from the owner.

- Trend Insight: Major manufacturers like Thales and payment networks (Visa/Mastercard) are currently piloting these cards globally.

- Virtual Smart Cards & Tokenization: Mobile wallets like Apple Pay and Google Wallet do not just store a photo of your card. They rely on EMV Payment Tokenisation to replace your actual card number with a unique digital “token.” The phone’s secure element then acts exactly like a contactless ICC, ensuring the real card details are never exposed to the merchant.

- Official Source: EMV Payment Tokenisation (EMVCo.com)

- eSIMs (Embedded SIM): The telecommunications industry is phasing out the removable SIM card in favor of the eSIM. This is a rewriteable chip built directly into the device’s motherboard, allowing users to switch carriers digitally without swapping physical plastic chips.

- Official Source: eSIM Specifications (GSMA.com)

9. Why Forex Traders Should Care About ICCs

While Integrated Circuit Cards are a general finance tool, understanding their mechanism is crucial for traders managing capital, specifically regarding operational risk and liquidity.

- Protecting Your Funding Source (Operational Risk): Forex traders rely on instant liquidity to fund accounts or meet margin calls. If you use an older magnetic stripe card for daily spending and it gets “skimmed,” your bank will freeze the account. An EMV chip card drastically reduces the chance of physical compromise, ensuring your funding channel remains active when you need it most.

- Security for “Digital Nomad” Traders: Many traders operate globally or use multi-currency accounts (like Wise or Revolut) to hold different currencies. These cards rely on advanced ICC technology to manage multiple currency “wallets” on a single chip, allowing secure spending and low-fee conversions while traveling.

- ATM Withdrawals of Profits: When withdrawing trading profits via an ATM, especially in foreign countries, the risk of “skimming” devices is real. A chip-enabled withdrawal ensures that even if a criminal installs a skimmer on the ATM, they cannot clone your card to steal your hard-earned profits.

10. Frequently asked questions about Integrated Circuit Card (ICC)

11. The Bottom Line

Integrated Circuit Cards (ICCs) are the global security standard for modern payments and digital identity.

By combining strong security with smart processing power, the ICC has effectively replaced the outdated and insecure traditional magnetic stripe card.

Even as technology moves toward digital IDs and eSIMs, the core Integrated Circuit Card technology remains the fundamental foundation for most secure transaction and identification systems used today. To see how FinTech innovations impact global markets, follow PipRider and read our latest Analysis.