Choosing a Forex broker can feel overwhelming, especially with so many options online. How do you know who to trust with your money? The answer lies in forex broker regulation. Think of regulators as the financial police force – government agencies that set strict rules brokers, acting as intermediaries, must follow to operate legally and ethically in the foreign exchange market.

Understanding these fx regulations is the single most important step you can take to protect yourself from scams and ensure a fair trading environment for speculative trading of foreign currency. This guide explains what regulation means, who the major players are (besides retail traders and brokers, large players like investment banks also participate in these financial markets), and how to check if your broker is legit.

Key Takeaways

- A system of rules set by financial authorities to ensure Forex brokers operate fairly and protect client funds.

- Regulation helps prevent fraud, ensures transparency, and provides traders with legal recourse if issues arise.

- Regulated brokers typically must keep client funds in separate accounts (segregation) and meet minimum capital requirements.

- Rules vary significantly worldwide; top-tier regulators (like FCA, ASIC, NFA) offer the strongest protection.

- Always verify a broker’s claimed forex license directly on the official regulator’s website before depositing funds.

1. What Is Forex Broker Regulation?

Forex broker regulation refers to the system of rules and oversight established by national or regional financial authorities to govern how Forex brokers operate. This concept, sometimes also called forex broker licensing or supervision, can be thought of as the rulebook and referee ensuring fair play in the massive global currency market.

The primary goals of these fx regulations are to:

- Protect Traders: Shield investors like you from fraud, manipulation, and unethical broker practices.

- Ensure Market Integrity: Maintain stability, transparency, and fairness in the Forex market, the world’s largest financial market with a daily trading volume reaching $9.6 trillion, according to the 2025 Triennial Central Bank Survey by the Bank for International Settlements (BIS).

- Safeguard Client Funds: Mandate that brokers keep trader deposits in segregated accounts, separate from the company’s operational funds. This protects your money if the broker becomes insolvent.

Essentially, regulation provides a crucial layer of security and accountability, making the Forex market safer for everyone involved. Without it, traders would have little protection against dishonest brokers.

2. U.S. Forex Brokerage Regulation

The United States has one of the strictest regulatory environments for Forex brokers globally. Is forex trading legal in the United States? Yes, absolutely, but it operates under tight supervision to protect traders. The goal is to create a transparent market and prevent manipulation.

2.1. Regulatory Bodies

Two main organizations oversee Forex brokers catering to US clients:

- Commodity Futures Trading Commission (CFTC): A federal agency that regulates the U.S. derivatives markets, including Forex futures and retail Forex trading. Its mission is to foster open, transparent, competitive, and financially sound markets.

- National Futures Association (NFA): A self-regulatory organization designated by the CFTC. All Forex brokers legally operating in the US must be registered members of the NFA. An NFA forex broker is subject to its strict rules and oversight. You can verify membership on the NFA’s website.

2.2. Key Rules for U.S. Retail Forex Trading

Several unique rules apply specifically to retail Forex traders in the US:

- Leverage Limit: The maximum leverage allowed for major currency pairs is capped at 1:50. This limits the potential risk exposure for retail traders but is significantly lower than what many international brokers offer, which fundamentally alters how margin calls work for US-based accounts in volatile markets.

- No Hedging Rule: Traders are not allowed to hold both a long and a short position in the same currency pair simultaneously in the same account. This FIFO rule affects how free margin is calculated since offsetting positions are not recognized.

- FIFO Rule (First-In, First-Out): If a trader has multiple open positions in the same currency pair, they must close the oldest position first when reducing their overall exposure. Under this FIFO rule, traders need careful position sizing strategies to avoid forced exits of profitable positions.

- Minimum Capital Requirement: According to the U.S. Code of Federal Regulations (17 CFR § 5.7), Retail Foreign Exchange Dealers (RFEDs) must maintain a minimum adjusted net capital of $20 million. This strict statutory mandate ensures they are financially stable and can meet their obligations to clients even during extreme market volatility.

These strict rules aim to protect retail traders from excessive risk and ensure brokers operate with high levels of financial integrity.

3. Essential Provisions in Forex Regulation

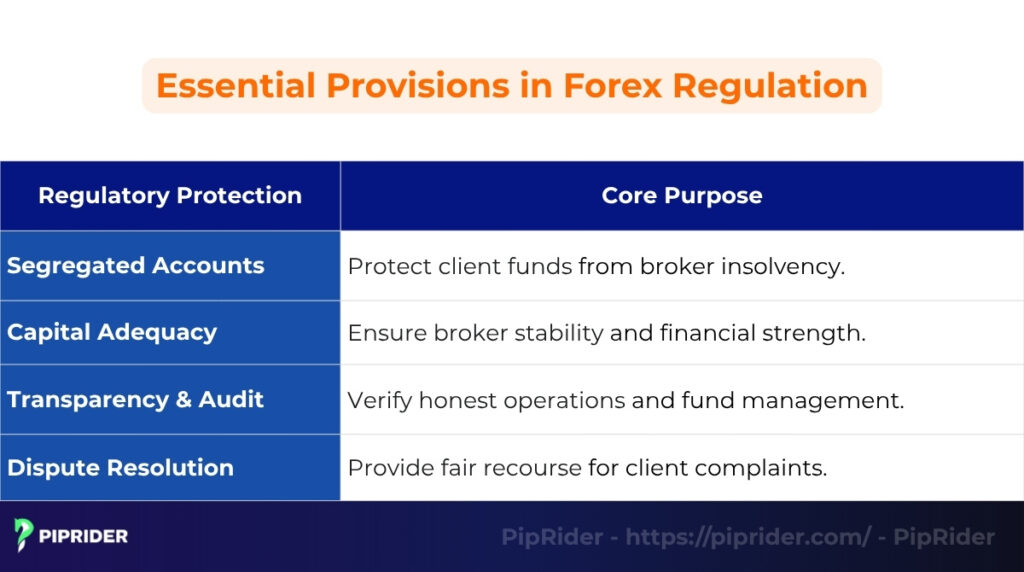

While rules vary globally, reputable forex broker regulation usually includes several core provisions designed to protect traders and ensure broker solvency. Understanding these helps you appreciate the value of trading with a well-regulated entity.

3.1. Segregated Client Accounts

This is arguably the most critical protection. Regulated brokers are required to hold client funds in segregated bank accounts, completely separate from the company’s own operational funds.

- Why it matters: If the broker goes bankrupt, your money is protected and cannot be used to pay the broker’s creditors. It ensures your deposits remain your property. This segregation requirement varies by jurisdiction and is one reason why choosing a properly regulated broker is crucial for capital safety.

3.2. Capital Adequacy Requirements

Regulators mandate that brokers maintain a specific minimum amount of operating capital at all times. This amount varies significantly depending on the jurisdiction (e.g., $20 million required by the NFA forex brokers in the US).

- Why it matters: This ensures the broker has sufficient financial resources to meet its obligations to clients and withstand potential market shocks without becoming insolvent.

3.3. Transparency & Audit Requirements

Regulated brokers must operate transparently and are subject to regular scrutiny.

- Requirements: This typically includes submitting regular financial reporting to the regulator and undergoing mandatory independent audits by external firms covering finances and transaction processes.

- Why it matters: Audits verify the broker’s financial health and compliance with regulations, ensuring they are operating honestly and managing client funds correctly.

3.4. Dispute Resolution Mechanisms

Reputable regulatory bodies provide clear avenues for traders to resolve disputes with their brokers regarding issues like client conduct.

- Mechanisms: This might involve an internal complaints process, mediation services, or an independent ombudsman scheme that can issue binding rulings or facilitate compensation.

- Why it matters: It gives traders recourse if they believe they have been treated unfairly, ensuring they have a way to seek resolution beyond dealing directly with the broker.

3.5. The Trader’s Protection Stack Summary

To quickly understand how these essential provisions apply in the real world, here is a summary of the “Protection Stack” mandated by top-tier regulatory authorities for retail CFD and Forex traders:

| Region (Regulator) | Client Money Segregation | Negative Balance Protection (NBP) | Compensation Scheme | Dispute Resolution / Ombudsman |

|---|---|---|---|---|

| UK (FCA) | Yes | Yes (FCA product intervention) | Yes (FSCS limits apply depending on product type) | Financial Ombudsman Service (FOS) |

| EU (CySEC, etc.) | Yes | Yes (ESMA mandate) | Yes (e.g., ICF in Cyprus, limits vary by state) | Local Financial Ombudsman |

| Australia (ASIC) | Yes | Yes (Introduced in 2021 rules) | No statutory scheme | Australian Financial Complaints Authority (AFCA) |

| US (NFA/CFTC) | Yes | Not statutorily mandated; however, strict NFA margin close-out rules effectively prevent accounts from reaching a negative balance in most cases | No | NFA Arbitration Program |

| Offshore (Tier 3) | Rarely guaranteed | No | No | Internal broker complaints only (High Risk) |

4. Differences in Regulations Around the World

Forex broker regulation is not uniform globally. The rules, leverage limits, and level of trader protection vary significantly from one jurisdiction to another within the global market. Understanding these differences is crucial when choosing a broker.

Here’s a comparison of key regulatory environments:

| Region | Key Regulator(s) | Key Traits | Max. Retail Leverage (Majors) | Notes |

|---|---|---|---|---|

| US | NFA / CFTC | Strictest oversight, $20M capital. | 1:50 | Strict enforcement of No Hedging and FIFO rules. Credit cards cannot be used to fund accounts. |

| UK | FCA | Strong protection, FSCS compensation (limits apply). | 1:30 | FSCS protects up to £85,000 per person per firm for investment-related claims (including Forex/CFDs). Always verify eligibility directly via fscs.org.uk. Post-Brexit, FCA licenses no longer offer passporting into the EEA. |

| EU | CySEC, BaFin etc. | Unified MiFID II framework. | 1:30 | Unified MiFID II framework. ‘Passporting rights’ allow a broker regulated in one EU state to legally accept clients from other EU countries only (excluding the UK). |

| Australia | ASIC | Strong enforcement, high compliance. | 1:30 | Previously allowed 1:500, but aligned with strict UK/EU leverage caps in early 2021 to protect retail traders. |

| Japan | FSA | Very strict limits, focus on domestic stability. | 1:25 | Highly isolated ecosystem; most FSA-regulated brokers only serve residents of Japan. |

| Singapore | MAS | Tier-1 Asian hub, strong AML/KYC rules. | 1:20 | Considered the most prestigious and secure regulatory hub in the Asia-Pacific region. |

| Offshore | FSC, SVGFSA etc. | Lower capital reqs, minimal oversight. | Up to 1:1000+ | High Risk. Leverage and protections depend entirely on the specific island nation’s loose laws. No compensation schemes. |

*Note: Leverage caps vary by product and client classification (e.g., retail vs. professional). The figures above refer specifically to common retail CFD and margin FX limits for major currency pairs.

As the table shows, major financial centers like the US, UK, EU, and Australia impose much stricter leverage limits (typically 1:30 to 1:50) compared to offshore jurisdictions, reflecting a greater focus on retail trader protection.

5. Global Forex Regulatory Authorities

Not all regulatory bodies offer the same level of protection. Experienced traders often categorize regulators into Tiers based on their strictness, enforcement history, and investor protection mechanisms. Understanding this hierarchy helps assess the real safety offered by a forex broker license.

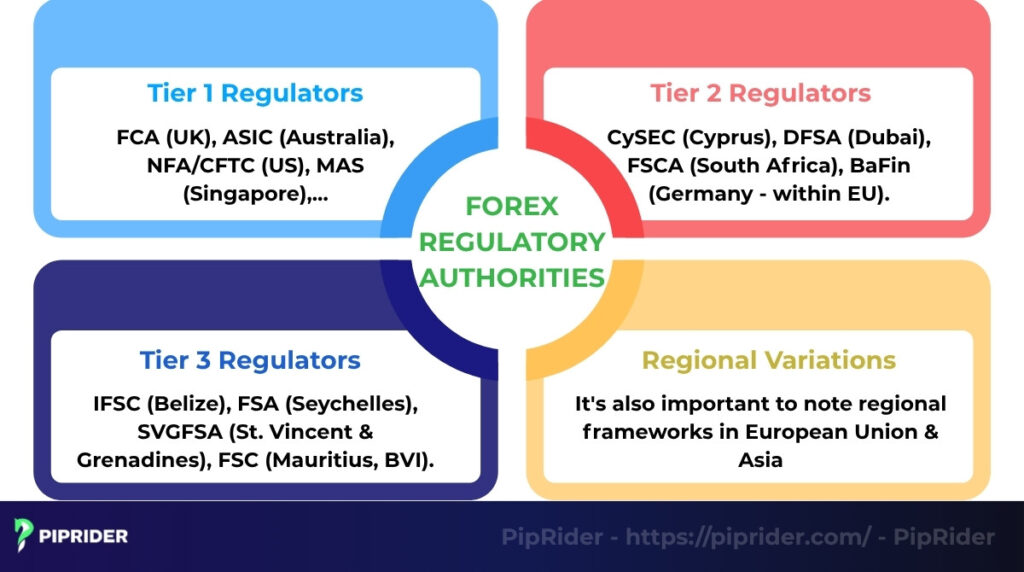

5.1. Tier 1 Regulators (Highest Trust & Protection)

These are the most stringent regulators, located in major, stable financial centers. They enforce strict rules, require high operating capital, offer investor compensation schemes, and actively monitor brokers. Brokers regulated here are generally considered the safest.

- Examples: FCA (UK), ASIC (Australia), NFA/CFTC (US), MAS (Singapore), FSA (Japan), FINMA (Switzerland).

5.2. Tier 2 Regulators (Moderate Trust & Protection)

These regulators provide a decent level of oversight but may have less stringent requirements or weaker enforcement compared to Tier 1. They often operate within established financial regions but might have lower capital requirements or limited compensation schemes.

- Examples: CySEC (Cyprus), DFSA (Dubai), FSCA (South Africa), BaFin (Germany – within EU).

Note: CySEC is categorized here as Tier 2 due to its history of more flexible enforcement compared to the FCA, despite operating under strict EU MiFID II standards.

5.3. Tier 3 Regulators (Low Oversight / Offshore)

These regulators are typically based in offshore jurisdictions. While they provide a license forex, their rules are often minimal, capital requirements low, and enforcement weak. Investor protection is very limited, making brokers regulated only in these regions significantly riskier.

- Examples: IFSC (Belize), FSA (Seychelles), SVGFSA (St. Vincent & Grenadines), FSC (Mauritius, BVI).

5.4. Regional Variations

It’s also important to note regional frameworks:

- European Union (EU): Brokers regulated within any EU member state (like CySEC in Cyprus or BaFin in Germany) generally must comply with the overarching MiFID II directive, which aims to harmonize investor protection standards across the bloc.

- Asia: Regulatory standards vary across Asia, but many jurisdictions are increasingly aligning with global best practices established by Tier 1 regulators.

Key takeaway: Always prioritize brokers regulated by Tier 1 authorities for the highest level of security.

Note on Prop Firms: This guide applies strictly to Forex Brokers (where you deposit your own capital). Funded Account providers (Prop Firms) operate under different legal structures and typically do not hold retail brokerage licenses.

6. How to Verify a Broker’s Regulation Status

Never take a broker’s word for granted regarding their regulation. Always perform due diligence yourself. Verifying a broker’s currency trading license is a simple but crucial process.

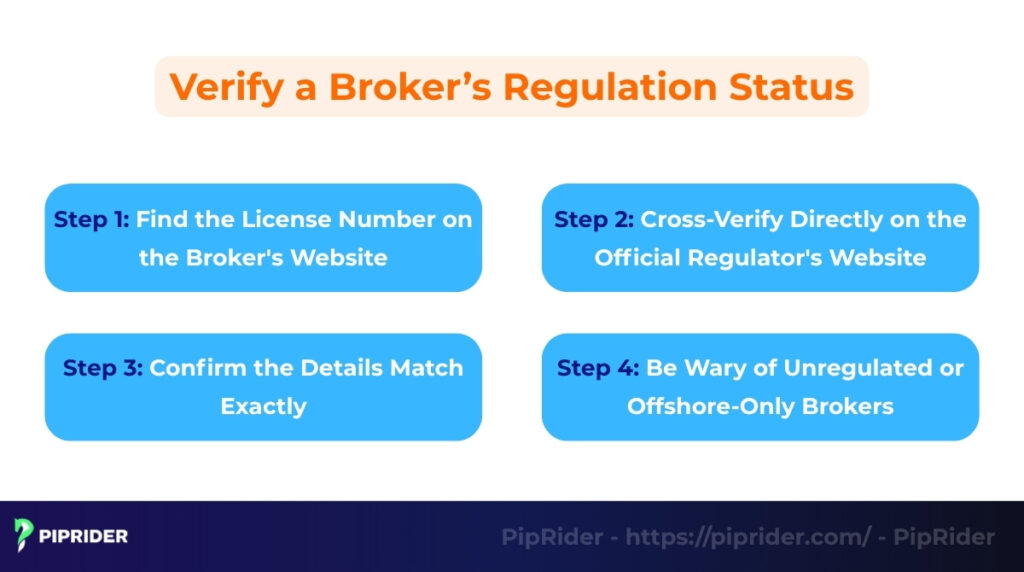

Step 1: Find the License Number on the Broker’s Website

Legitimate, regulated brokers will always display their license number(s) and the name(s) of their regulator(s) clearly on their website.

- Where to look: Usually found in the footer (bottom) of every page, or on an “About Us” or “Regulation” page.

- What to note: Write down the exact legal name of the company operating the broker and its license/registration number.

Step 2: Cross-Verify Directly on the Official Regulator’s Website

This is the most critical step. Do not trust links provided by the broker to avoid sophisticated phishing scams. Always type the regulator’s name into a search engine yourself to find their official public database.

Key Regulator Search Terms (Type these into Google):

- FCA (UK): Search for “FCA Financial Services Register”

- ASIC (Australia): Search for “ASIC Professional Registers”

- NFA (US): Search for “NFA BASIC lookup”

- CySEC (Cyprus): Search for “CySEC Approved Investment Firms Register”

Action: Once on the official site, search using the license number or the company’s legal name.

Step 3: Confirm the Details Match Exactly

Once you find the listing on the regulator’s site, ensure the details match perfectly:

- Legal Entity Name: Is the company name listed by the regulator identical to the one operating the website? Small variations can indicate a different, possibly unrelated entity.

- Approved Domains: Some regulators (like the FCA) list the approved website domains associated with the license. Ensure the broker’s website you are using is listed.

- License Status: Is the license currently active and authorized? Or is it expired, suspended, or revoked?

Step 4: Be Wary of Unregulated or Offshore-Only Brokers

If you cannot find the broker on the claimed regulator’s website, or if they are only regulated in a Tier 3 (offshore) jurisdiction, treat this as a major red flag.

- Warning Signs: Be extremely cautious. Many scams involve “cloning” the details of legitimate brokers or using entirely fake forex license information. Unregulated forex brokers offer virtually no protection for your funds.

6.1. The “Entity Trap”: Where Your Protection Actually Lies

A common mistake for beginners is assuming that if a broker “is regulated by the FCA,” all their accounts are protected by the FCA. This is rarely the case.

Brokers often operate through multiple legal entities across different jurisdictions. Your level of protection, including leverage limits, NBP, and compensation schemes, depends entirely on the specific entity stated in your account agreement.

Crucial Check: Always check the footer of the broker’s website or your client agreement. If you are a resident of the EU but the broker signs you up under their “Global” (offshore) entity, you will lose all Tier-1 regulatory protections.

6.2. Verify in Practice: How to Read the Regulators’ Registers

Telling you to “verify” is one thing; showing you how to read the complex regulatory databases is another. To fulfill the practical intent of this guide, here is a mini-tutorial on verifying brokers across the top-tier regulators: the FCA (UK), ASIC (AU), and NFA/CFTC (US).

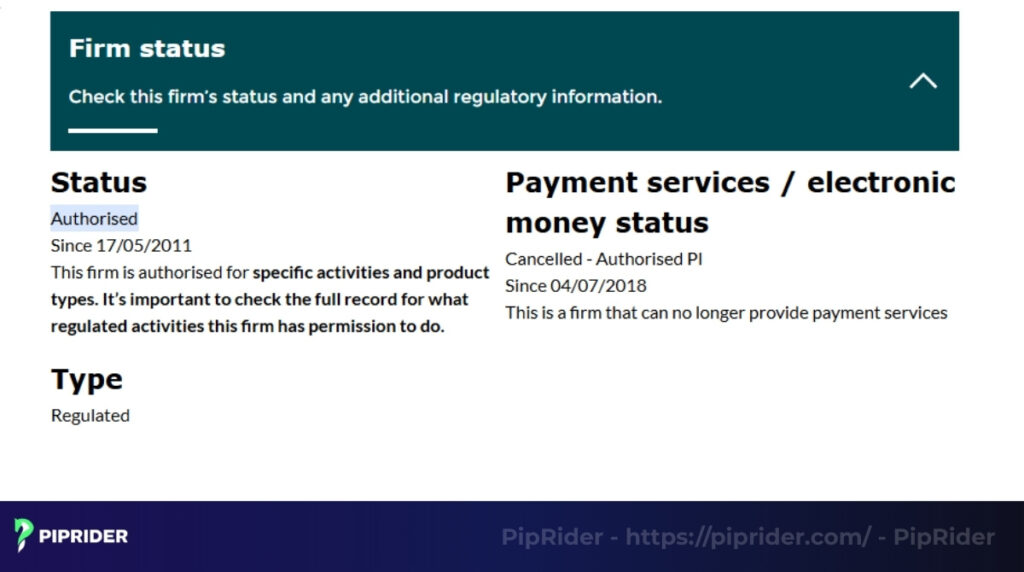

Tutorial 1: The UK’s FCA Financial Services Register

The FCA register is highly detailed. A simple “Authorised” status is not enough; you must verify their specific permissions.

Verification Checklist:

- Firm Status: Must explicitly state “Authorised”. Be highly suspicious of “EEA Authorised” (often just a passporting right) or “Appointed Representative” (piggybacking on another firm’s license).

- Anti-Clone Check: Scammers frequently clone real Firm Reference Numbers (FRNs). You must cross-reference the registered phone number and website domain on the FCA register with the broker’s actual website. If they do not match exactly, walk away.

- Permissions & Customer Type: Scroll to the “Permissions” section. Look for “Rolling spot forex contract” or “Contract for Differences”. Crucially, click on these permissions to ensure the “Customer Type” includes “Retail”. If it is restricted to “Professional” or “Eligible Counterparty,” retail traders have no regulatory protection.

Tutorial 2: Australia’s ASIC Professional Registers

When verifying an Australian broker, you must search the “AFS Licensees” register, not just the general company directory.

Verification Checklist:

- Status: Must show “Current”.

- License Type: Ensure they hold an Australian Financial Services Licence (AFSL). A standard ACN (Australian Company Number) is merely a corporate registration and offers zero financial oversight.

- The Retail Trap (Authorisations): Read the “Authorised to provide financial product advice” section carefully. It must list “Derivatives” and “Foreign Exchange Contracts”. More importantly, it must state authorization to provide these services to “Retail Clients”. Many unregulated entities use a “Wholesale Clients” AFSL to illegally onboard retail traders.

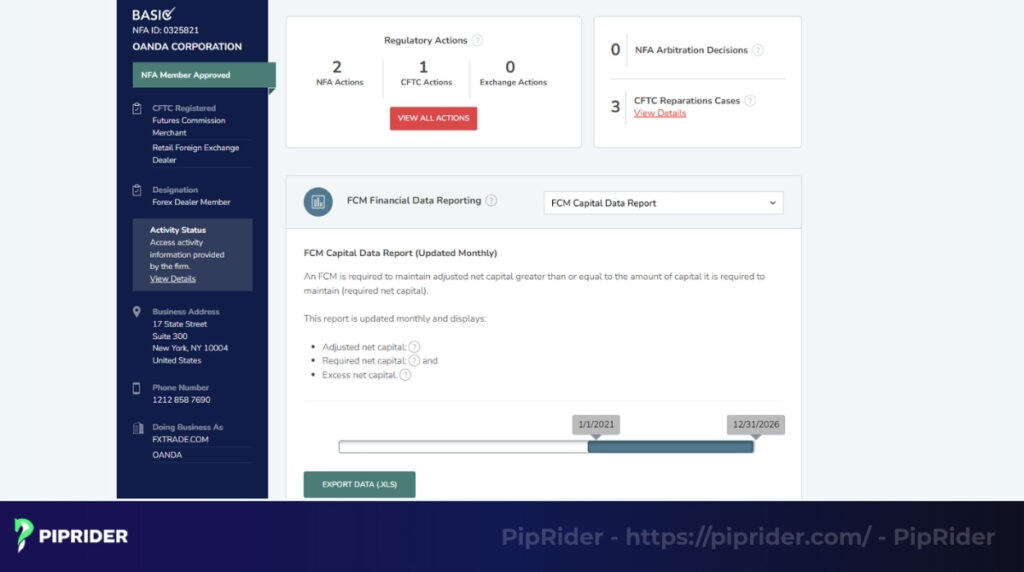

Tutorial 3: The US’s NFA BASIC (via CFTC “Check”)

The US regulatory environment is the most stringent. The correct verification path is to start at the CFTC’s dedicated background check portal (cftc.gov/check), which feeds directly into the NFA BASIC database.

Verification Checklist:

- Current Status: The profile must clearly state “NFA Member Approved”.

- Firm Regulatory Categories: To legally offer margin Forex to retail US clients, the broker MUST be registered as a Retail Foreign Exchange Dealer (RFED) and typically a Futures Commission Merchant (FCM).

- Regulatory Actions: Scroll to the bottom of the BASIC profile. An optimal broker has “0 found” under Regulatory Actions. Any listed CFTC or NFA enforcement actions, fines, or disciplinary histories are severe red flags regarding operational integrity and client fund management.

7. The “Red Flag” Checklist: Critical Warning Signs

In the financial world, transparency is mandatory. Any discrepancy in a broker’s regulatory claims is a non-negotiable red flag. Before committing your capital, cross-reference this “Red Flag” checklist:

Technical Discrepancies (High-Level Scams)

- Domain Mismatch: The broker claims a Tier-1 license, but the URL you are using (e.g.,

trading-fca-secure.com) is not listed as an approved domain on the official regulator’s register. This is a classic Clone Firm tactic. - Entity Name Arbitrage: The regulator lists “Broker XYZ Pty Ltd,” but your account agreement is with “Broker XYZ Ltd.” Scammers use near-identical names to divert clients to unregulated offshore entities without their knowledge.

- Non-Governmental “Regulators”: Be skeptical of licenses from self-proclaimed bodies like the “International Financial Market Board.” Genuine regulators are always established by national governments (e.g., FCA, ASIC, CFTC).

Operational Red Flags

- Guaranteed Returns: Forex is inherently risky. Any promise of “guaranteed profits” or “no-loss systems” is a violation of Tier-1 marketing rules and a hallmark of a Ponzi scheme.

- Unconventional Withdrawal Requirements: If a broker demands “advance taxes” or extra fees before allowing a withdrawal, they are likely attempting to extract more funds before disappearing.

- Listed on Official Warning Lists: Before depositing, search the “Warning List” or “Unauthorised Firms” list of the FCA or ASIC. If the broker is named there, do not engage.

- Opaque Legal Information: A legitimate broker provides a clear legal entity name and license number in their website’s footer. If this is missing or intentionally vague, walk away.

8. Frequently asked questions about Forex Broker Regulation

9. The Bottom Line

Forex broker regulation is the absolute foundation for choosing a safe and reliable trading provider. It’s the primary factor that protects you from potential fraud and ensures fair trading conditions in the wider financial markets.

For the maximum level of security and investor protection, always prioritize providers overseen by Tier-1 regulators such as the FCA (UK), ASIC (AU), or the NFA/CFTC (US). Crucially, never take their claims at face value. Always take the extra minute to verify their forex license and legal entity directly on the official regulator’s website, and steer clear of unlicensed or offshore-only providers entirely.

PipRider continuously provides provider insights and regulation updates to empower your safe trading strategies and deepen your market understanding.