A Guaranteed Investment Fund (GIF) is a special investment product sold only by life insurance companies. Think of it as a hybrid that combines the growth potential of a mutual fund with the safety net of an insurance policy.

The main feature of a GIF financial product is its promise, or “guarantee.” It ensures that at a future date (called maturity) or upon death, you (or your heirs) will receive back at least 75% or 100% of your initial investment, regardless of how the stock market has performed. This article explains what is a Guaranteed Investment Fund, how it works, and its major pros and cons.

Key Takeaways

- A GIF is an insurance contract that invests your money in segregated funds, which behave like mutual funds.

- It guarantees to return 75% or 100% of your initial deposit, but only at maturity (usually 10-15 years) or upon death.

- GIFs have significantly higher fees (MERs) than traditional mutual funds because you are paying for the insurance guarantee.

- Unlike mutual funds, GIF assets can bypass probate and be paid directly to your named beneficiaries, saving time and fees.

- This product is designed for very conservative, long-term investors (like those nearing retirement) who prioritize capital protection over high returns.

1. What Is a Guaranteed Investment Fund (GIF)?

A Guaranteed Investment Fund (GIF) is a hybrid investment product sold by insurance companies that combines the growth potential of a mutual fund with the safety of an insurance contract (Avenue Investment Management, 2025).

In the Canadian market, these products are legally known as Segregated Funds (or “Seg Funds”). It is crucial to distinguish them from “Capital Protected Funds” in the UK or other US-based products. As the name implies, the assets are “segregated” (held separately) from the insurance company’s general funds to protect the investor.

The defining feature of a Guaranteed Investment Fund is its capital guarantee This contract promises that the investor (or their beneficiaries) will receive at least 75% to 100% of their initial investment back (GetSmarterAboutMoney.ca, 2023). This guarantee applies only upon the contract’s maturity date (often 10-15 years) or upon the investor’s death, even if the underlying market investments have lost value.

Functionally, the money is invested in underlying funds that look and feel like mutual funds, but with the added insurance wrapper. The primary goal is capital protection, making it an investment vehicle for conservative investors who want market exposure but fear losing their initial investment.

⚠️ Important: GIF vs. GIC – Don’t Confuse Them

It is crucial not to mistake a Guaranteed Investment Fund (GIF) for a Guaranteed Investment Certificate (GIC). While both offer “guarantees” and sound similar, they are fundamentally different products sold by different institutions (Sun Life Global Investments, n.d.).

- GIC (Bank Product): You lend money to a bank. Your return is a fixed interest rate known in advance. Your principal is protected from day one.

- GIF (Insurance Product): You invest in the market via an insurance contract. Your return is variable (based on market performance). Your principal is protected only at maturity or death.

2. How Guaranteed Investment Funds Work

Unlike buying a stock directly, investing in a Guaranteed Investment Fund (GIF) involves entering into a legal agreement with an insurance company. The mechanism works by wrapping a standard investment portfolio within an insurance policy to protect the principal.

2.1. Structure and Components

To truly understand how a GIF protects your money, you need to look at its internal architecture. The product is not a single asset but is built on three distinct layers that work together:

- The Contract: The investor signs a life insurance contract and deposits a lump sum (the premium). This legal wrapper is what provides the estate planning benefits.

- The Investment: The insurance company places this money into segregated funds (kept separate from the company’s assets). These funds hold a mix of stocks and bonds to generate market growth, similar to a mutual fund.

- The Guarantee: The insurance layer provides a specific promise to protect the principal (75% or 100%) at maturity or death, ensuring safety regardless of market performance.

2.2. Maturity and Death Benefit Guarantees

It is critical to note that the capital protection is not “always on” like a bank account. The guarantee is conditional and typically activates strictly in two specific scenarios:

- Maturity Guarantee: This guarantee applies only if you hold the contract for a fixed term, commonly 10 years (though some contracts range up to 15 years or age 100). If the market value is lower than your guaranteed amount at this specific maturity date, the insurer pays the difference.

- Death Benefit Guarantee: If the investor dies before the maturity date, their named beneficiary receives the guaranteed amount or the current market value, whichever is higher.

2.3. Fees and Conditions: The True Cost

This added layer of security comes at a premium. Because you are purchasing both an investment vehicle and an insurance policy, the fee structure is distinct and impacts your returns heavily:

- Higher MER (The Fee Drag): GIF fees (MER) are typically 2.5% to 3.5%, often significantly higher than comparable mutual funds due to the insurance cost (GetSmarterAboutMoney.ca, 2023). This “insurance cost” compounds over time, creating a drag on your growth.

- Example: On a $50,000 investment over 10 years (assuming a 5% gross market return):

- Mutual Fund (2% fee): You earn a net 3%. Final value ≈ $67,195.

- GIF (3% fee): You earn a net 2%. Final value ≈ $60,950.

- The Cost: You sacrificed over $6,000 in potential growth just to pay for the guarantee.

- Impact on Guarantee: Crucially, withdrawals reduce your guaranteed amount proportionately, not just by the dollar amount withdrawn. If you withdraw 10% of your current account value, your guaranteed principal also drops by 10%. This can significantly lower your safety net if you access funds when the market is down.

2.4. The “Reset Option” (And Its Catch)

One of the most unique features of segregated funds is the “Reset Option,” which allows investors to lock in market gains. However, this feature acts as a double-edged sword regarding your timeline:

- The Benefit: If your $100,000 investment grows to $120,000, you can reset the guarantee to protect this new $120,000 value.

- The Catch (Reset Clock): Crucially, exercising this option usually resets the maturity clock. For example, if you have a 10-year contract and use the reset option in Year 3, your new 10-year countdown begins from that date, locking your capital up for a longer period.

⚡ Reality Check: How the Guarantee Really Works

Before investing, understand that the “100% guarantee” has strict conditions:

- Not “Always On”: The guarantee triggers only at the maturity date (commonly 10 years) or upon death. If you cash out earlier, you get the current market value, which may be a loss.

- The Reset Trade-off: While “locking in gains” sounds good, using the Reset Option typically restarts the maturity clock. A 10-year wait becomes a new 10-year wait.

- It Can Shrink: The guarantee is not absolute. Any early withdrawal will proportionately reduce your guaranteed amount. You cannot withdraw cash and expect the remaining guarantee to cover 100% of your original deposit.

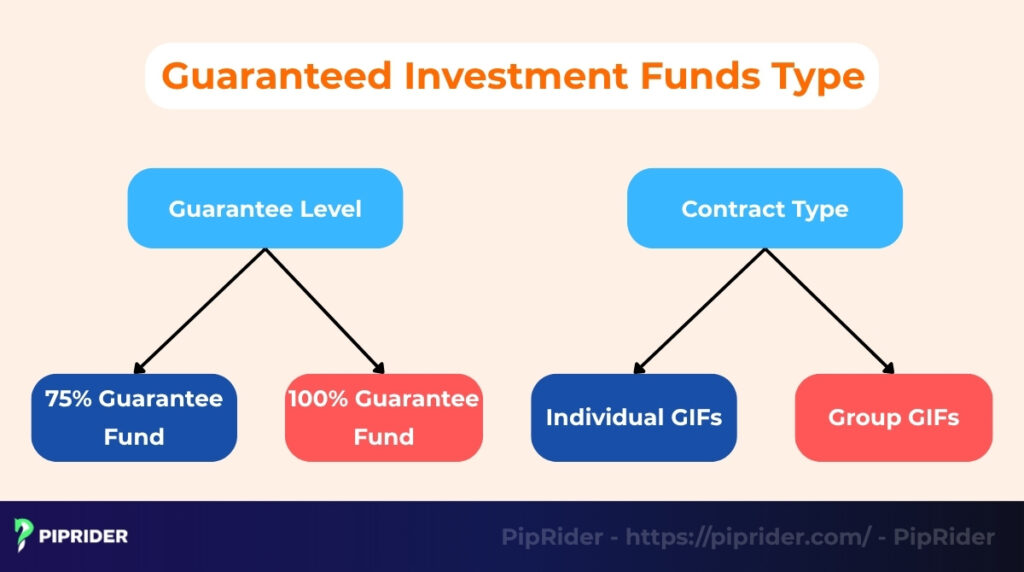

3. Types of Guaranteed Investment Funds

Guaranteed Investment Fund (GIF) contracts are not all the same. They are primarily categorized by their guarantee level and contract type, which determine their cost and flexibility.

3.1. By Guarantee Level

The “guarantee” is the main feature, and it comes in two common levels:

- 75% Guarantee Fund: This is the most common type. It guarantees that at maturity or death, you will receive at least 75% of your initial investment. Because the guarantee is lower, these funds typically have lower fees and may offer more investment flexibility. They are often used for medium-to-long-term goals where some growth is still a priority.

- 100% Guarantee Fund: This type offers maximum safety, guaranteeing that you will receive 100% of your initial investment back at maturity or death, regardless of market performance. This “peace of mind” comes at a cost, as these funds have higher fees, which can reduce overall returns. They are best suited for very conservative investors or those near retirement who cannot afford to lose any principal.

3.2. By Contract Type

GIFs are also structured as either individual or group plans:

- Individual GIFs: This is a standalone contract purchased by an individual investor. It offers the most flexibility, allowing the investor to choose their specific funds, guarantee levels, and beneficiaries according to their personal financial plan.

- Group GIFs: These are offered as part of a larger plan, such as a company pension plan or a group retirement savings plan. The investment options and features are chosen by the plan sponsor, so there is less individual flexibility.

4. Key Features and Concepts

Guaranteed Investment Fund (GIF) contracts have unique legal structures that differentiate them from standard mutual funds. These features stem directly from their classification as insurance contracts.

4.1. Maturity and Death Guarantees

This is the product’s foundation. As detailed in Section 2, the contract guarantees that 75% to 100% of your principal will be returned. However, remember that this safety net is time-dependent: it only applies on the specific maturity date (e.g., after 10 years) or upon the death of the annuitant.

4.2. Estate Bypass (Probate Bypass)

This is arguably the most powerful feature for estate planning. Because a GIF is an insurance policy with a named beneficiary, the death benefit is paid directly to the beneficiary, bypassing the estate.

- The Benefit: This allows heirs to avoid probate fees (which can be high in some provinces) and receive funds much faster (often within weeks, compared to months or years for an estate settlement).

- Privacy: Unlike a will, which becomes a public record during probate, insurance payouts remain private.

4.3. Potential Creditor Protection

Because GIFs are insurance contracts, assets may be protected from creditors in the event of bankruptcy or lawsuits. This potential protection makes them attractive to business owners and professionals in high-liability fields.

- Important Constraint: This protection is not automatic. It depends strictly on proper beneficiary designations (typically requiring a “family class” beneficiary like a spouse or child) and varies by provincial law.

- Legal Advice Required: Never assume you are protected. You must seek professional legal advice to ensure your contract structure meets the necessary legal criteria for creditor protection.

4.4. Tax Treatment (Depends on Account Type)

Taxation for GIFs is not “one size fits all”; it depends entirely on whether the contract is held in a registered or non-registered account.

- Registered Accounts (RRSP, TFSA): If you hold a GIF inside an RRSP or TFSA, the tax rules of that plan apply. Growth is tax-sheltered (RRSP) or tax-free (TFSA), and you generally do not report annual income.

- Non-Registered Accounts: Contrary to common belief, you do not get total tax deferral. Even if you don’t withdraw money, the fund generates income allocations (interest, dividends, or capital gains) each year. These are allocated to you to keep the fund tax-neutral. You will receive a T3 slip and must pay taxes on this allocated income annually (Sun Life Global Investments, n.d.).

Disclaimer: Tax treatment can be complex and may vary by province or specific contract terms. Always consult a tax professional.

4.5. Liquidity Windows (Free Withdrawal Limit)

While GIFs are long-term contracts with surrender penalties, most offer a “Free Withdrawal Limit.” This clause typically allows you to withdraw a specific percentage (e.g., 10% of the account value) once per calendar year without paying a surrender fee. However, keep in mind that any withdrawal will proportionately reduce your guaranteed principal amount.

5. Guaranteed Investment Funds vs. Mutual Funds

While GIFs (also known as Segregated Funds) and Mutual Funds both pool money from investors, they are fundamentally different products. GIFs are insurance contracts that offer guarantees, while Mutual Funds are purely investment products.

Here is a direct comparison:

5. Comparison: Guaranteed Investment Funds vs. Mutual Funds

While both vehicles pool money from investors, they serve different purposes. Here is the direct breakdown:

| Feature | Guaranteed Investment Fund (GIF) | Mutual Fund |

|---|---|---|

| Capital Protection | Yes (Guarantees 75% or 100% at maturity/death) | No (Principal is fully at risk) |

| Estate Benefit | Bypasses Probate (Paid directly to beneficiary; private) | Subject to Probate (Becomes part of the estate; public) |

| Fees (MER) | Higher (Includes insurance cost, creating “fee drag”) | Lower (More of your money works for you) |

| Impact of Withdrawals | ⚠️ Proportionately Reduces Guarantee (Early withdrawal lowers your guaranteed amount) |

Dollar-for-Dollar (Reduces account balance only) |

| Creditor Protection | Potential (Available for business owners/professionals) | None |

| Best For | Estate Planning & Protection (Seniors, Conservative Investors, Business Owners) |

Wealth Accumulation (Long-term growth investors seeking lower fees) |

In short, investors in a Guaranteed Investment Fund pay significantly higher fees in exchange for capital protection and estate benefits. Investors in a Mutual Fund accept full market risk in exchange for lower fees and higher growth potential.

For those looking for even lower management costs, comparing mutual funds and ETFs can provide a broader perspective on how different structures impact long-term wealth accumulation.

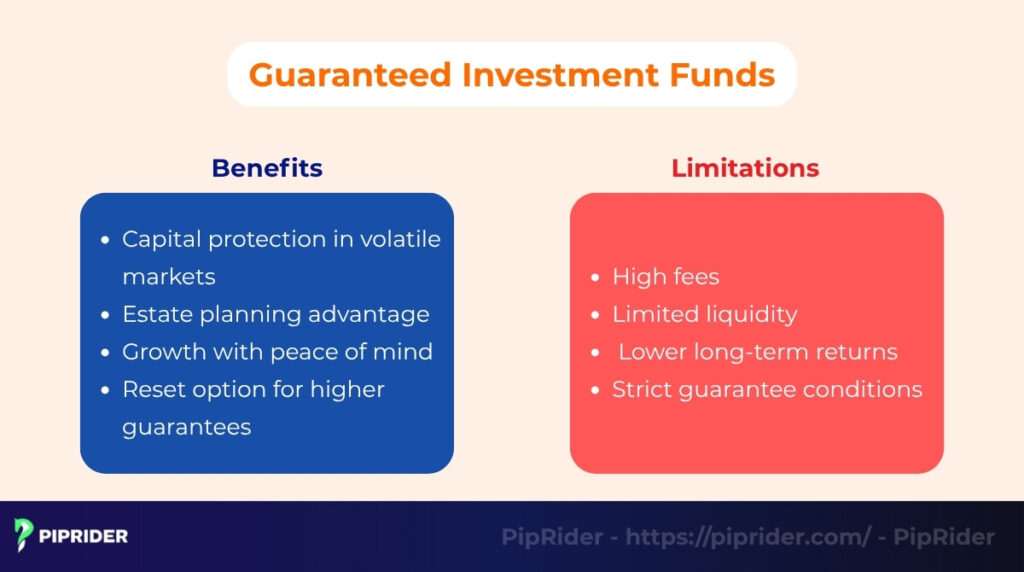

6. Benefits of Guaranteed Investment Funds

Guaranteed Investment Fund (GIF) contracts offer several specific advantages, primarily centered on security and estate planning rather than maximum returns.

- Capital protection in volatile markets: The main benefit is the guarantee itself. This provides a safety net during severe market downturns, ensuring that even in a crash, a significant portion (75% or 100%) of the investor’s principal is protected at maturity or death.

- Estate planning advantage (Probate Bypass): GIFs act as a powerful estate planning tool. By naming a specific beneficiary on the contract, the funds bypass the probate process and are paid directly to the heir.

- Note: This avoids potential legal delays and high probate fees in provinces like Ontario or B.C. However, in Quebec, where probate fees are generally not applicable for notarial wills (Éducaloi, n.d.), the cost benefit is lower, though the advantages of speed and privacy remain.

- Growth with peace of mind: These funds allow conservative investors to participate in market growth (from stocks and bonds) without accepting the full downside risk. It offers a psychological benefit, providing “peace of mind” that the initial capital is protected.

- Reset option for higher guarantees: The reset option allows investors to lock in market gains. If the fund’s net asset value increases, the investor can reset the guarantee to the new, higher value, effectively protecting their profits as well as their principal (keeping in mind this usually resets the contract maturity date).

7. Risks and Limitations

While GIFs offer unique protections, they come with significant costs and trade-offs. It is crucial to understand these limitations before investing.

- High fees: This is the most significant drawback. GIFs have a much higher Management Expense Ratio (MER) than standard mutual funds. This extra cost pays for the insurance guarantee and management, which can substantially reduce your net asset value and net returns over time.

- Limited liquidity: GIFs are long-term products, not emergency funds. If you withdraw your money before the maturity date, you will likely face steep surrender charges (penalties), and, in most cases, you will lose the capital guarantee on the amount you withdraw.

- Lower long-term returns: The “cost of the guarantee” (the high fees) creates a drag on performance. Because safety is the priority, the net returns from a Guaranteed Investment Fund are often lower than what you might earn from a standard balanced mutual fund or a simple portfolio of stocks (equity) and bonds over the same period.

- Strict guarantee conditions: The capital protection is not available at all times. The 75% or 100% guarantee only applies on two specific dates: the contract’s maturity date (often 10-15 years away) or upon the investor’s death. If you need your money on any other day, you will only get the current market value (the fund’s net asset value), which could be less than your principal.

8. Who Should Invest in Guaranteed Investment Funds?

A Guaranteed Investment Fund (GIF) is a niche investment vehicle designed for a very specific type of investor. It is not suitable for most people, especially short-term traders or those seeking high returns.

GIFs are most appropriate for:

- Pre-Retirees and Retirees: Individuals nearing or in retirement whose primary goal is capital protection. They cannot afford to lose their principal savings and are willing to pay for the guarantee.

- Very Conservative Investors: People with a low-risk tolerance who prioritize stability and peace of mind over maximizing returns.

- Individuals Focused on Estate Planning: The ability to bypass probate and pass assets directly to a beneficiary makes GIFs a useful tool for estate transfer or protecting a financial legacy for an heir.

This product is not suitable for short-term traders, young investors with a long time horizon, or anyone whose main goal is achieving high market returns.

When planning for retirement, it’s worth comparing guaranteed investment funds with home equity lending options each offers different trade-offs between safety, liquidity, and legacy value.

9. How to Invest in Guaranteed Investment Funds

To invest in a Guaranteed Investment Fund (GIF), you must follow a specific process distinct from buying stocks. Since these are insurance contracts, they are sold exclusively through licensed channels, not on DIY trading apps.

9.1. Step 1: Find a Licensed Advisor

Because GIFs are regulated insurance products, you cannot simply purchase them through a standard brokerage account. You are required to work with a qualified professional who holds a Life Insurance License (LLQP) to ensure the product is suitable for your financial situation.

- Where to look: You can engage an independent insurance broker or a financial planner at your bank. Note that while many bank advisors are dual-licensed (mutual funds + insurance), you should specifically ask for someone qualified to sell segregated funds.

9.2. Step 2: Compare Fees and Providers

GIFs are issued by Canada’s major insurance carriers (e.g., Sun Life, Manulife, Canada Life), but not all contracts are created equal. Conducting due diligence is essential before committing your capital.

- Action: Compare the MERs (Management Expense Ratios) and the fund selection. Fees can vary significantly between providers, and you want to ensure the contract offers high-quality underlying funds that match your investment goals.

9.3. Step 3: Choose Your Guarantee Level

Most providers offer tiered options, requiring you to make a strategic trade-off between cost and safety. You will typically need to select one of the following structures:

- 75/75 Guarantee: Protects 75% of principal at maturity and 75% at death. This option typically carries lower fees (MER) and is better for investors seeking higher growth potential.

- 100/100 Guarantee: Protects 100% of principal at both maturity and death. This offers maximum safety but comes with higher MERs and often places stricter limits on how much equity (stocks) you can hold.

9.4. Step 4: Sign and Designate a Beneficiary

The final stage involves reviewing the “Information Folder” (the insurance equivalent of a prospectus) and signing the application. This is the moment to formalize your estate planning strategy.

- Critical Step: You must designate a named beneficiary (e.g., spouse, child) on the application form.

- Why: If you leave this blank or name “The Estate,” you will lose the probate bypass benefit and potential creditor protection discussed in Section 6.

10. Alternatives to Guaranteed Investment Funds

A Guaranteed Investment Fund (GIF) is a very specific investment vehicle. For investors seeking safety or growth, there are several common alternative investment vehicle options that may be more suitable.

10.1. GICs (Guaranteed Investment Certificates)

Similar to a Certificate of Deposit (CD) in the U.S., a GIC is a very safe investment offered by banks.

- How it works: You lend the bank a sum of money for a fixed term (e.g., 1-5 years) in exchange for guaranteed returns at a fixed interest rate (a fixed yield).

- Key difference: GICs offer total capital safety and a predictable return, but they have no potential for market growth. A GIF offers less safety (a variable yield) but some potential for market growth.

On the other hand, investors who prioritize immediate access without any lock-up period may prefer high-yield savings accounts, which provide a straightforward option for short-term security.

10.2. Balanced Mutual Funds

These are standard investment funds, like a balanced mutual fund or index fund, that offer a diversified mix of stocks (equity) and bonds (e.g., 60% stocks, 40% bonds).

- How it works: They provide market exposure and growth potential but carry market risk.

- Key difference: Balanced funds have higher risk (you can lose principal) but also higher potential long-term returns and lower fees (MERs) than a GIF because you are not paying for an expensive insurance guarantee.

10.3. Annuities

Annuities are also insurance contracts, but their primary goal is different. A guaranteed income fund (or annuity), such as the Prudential Guaranteed Income Fund, is designed to provide a stable, predictable income stream for life.

- How it works: You pay a lump sum to an insurance company, and in return, they pay you a fixed amount of money every month or year for the rest of your life.

- Key difference: An annuity’s main purpose is to create income, not grow capital. Most annuities do not offer market upside (growth) in the same way a GIF does.

11. Regulation and Policyholder Protection

Unlike mutual funds, which are regulated by securities commissions, Guaranteed Investment Funds are insurance contracts regulated by provincial insurance bodies. This distinction ensures specific consumer protections.

11.1. Provincial Regulation (Example: AMF)

Each province has a dedicated regulator to oversee these products. For instance, in Quebec, the Autorité des marchés financiers (AMF) strictly enforces that insurers must provide clear documentation—specifically an “Information Folder” and “Fund Facts”—so investors fully understand the fees, guarantees, and risks before signing (Autorité des marchés financiers, n.d.).

11.2. Assuris Protection (If the Insurer Fails)

A common question from investors is: “What happens to my guarantee if the insurance company goes bankrupt?”

In Canada, your segregated fund contract is protected by Assuris, a non-profit organization designated to protect policyholders in the event of insurer insolvency.

- The Coverage: Assuris guarantees that policyholders will retain a significant portion of their promised benefits. Protection limits were recently increased:

- Death Benefit: Protected up to 100% of amounts up to $200,000 (or 90% for higher amounts).

- Maturity Guarantee (Investment): Protected up to 100% of amounts up to $100,000 (or 90% for higher amounts) (Newswire, n.d.).

- Recommendation: Since protection limits can change over time, investors should always verify the latest coverage details directly on the Assuris website.

12. Frequently asked questions about Guaranteed Investment Fund

13. The Bottom Line

A Guaranteed Investment Fund (GIF) represents a compromise, offering a middle ground between capital safety and potential market growth.

While the long-term returns (reflected in the net asset value) are often lower than traditional mutual funds due to high fees, a GIF provides psychological stability and clear estate planning benefits. It is best suited for conservative investors who prioritize safety over speculation, especially during periods of high market volatility.

To learn how market volatility impacts different assets, follow PipRider and check out our latest market Analysis.