While standard banks offer as low as 0.01%, saver accounts with high interest (HYSAs) now provide yields up to 5.00% APY (Bankrate, 2026), over 10x to 12x the national average (Federal Deposit Insurance Corporation [FDIC], 2026). For traders, these accounts are the ideal place to park “dry powder,” earning risk-free returns while maintaining liquidity for market opportunities.

As of January 2026, HYSAs offer a safe, FDIC-insured haven for emergency funds. However, unlike CDs, APYs are variable and fluctuate based on Federal Reserve policy. This guide ranks the best options for 2026 based on rates, fees, and transfer speed.

Key Takeaways

- Earn more Interest: HYSAs offer much higher Annual Percentage Yields (APYs) than regular savings accounts.

- Safe & Secure: Funds are typically insured by the FDIC (banks) or NCUA (credit unions) up to $250,000.

- Good for goals: Ideal for emergency funds, down payments, or other short-to-medium-term savings goals.

- Online banks lead: The best savings yields are often found at online banks due to lower overhead costs.

- Rates fluctuate: APYs can change based on Federal Reserve policy and market conditions, so compare regularly.

Why Every Trader Needs a High-Interest Saver Account

In trading, cash is a position. A high-yield account serves two critical purposes for your portfolio:

- Capital Preservation: It protects your emergency fund from market volatility.

- Dry Powder Efficiency: It generates a “risk-free” return on cash waiting for a high-probability trade setup, ensuring your money never stays unproductive.

1. What Is a High-Interest Savings Account?

A high-yield savings account (also called a HYSA) is a type of savings account offering significantly higher interest rates than traditional ones. It works just like a regular account. Your money is kept safe (usually FDIC/NCUA insured) and accessible, but it earns interest at a much faster rate, often many times the national average.

The key difference is the Annual Percentage Yield (APY). While standard savings accounts might offer minimal interest, HYSAs provide a much better return, making them ideal for growing your cash reserves faster.

These accounts are particularly well-suited for:

- Building an emergency fund, which is essential for separating trading capital from emergency savings to ensure your daily living expenses remain untouched by market volatility.

- Saving for short-to-medium-term goals (like a down payment or vacation).

- Anyone seeking safe, steady growth for their cash without investment risk.

📈 The Trader’s Protocol: Separating “Alpha” from “Safety”

For active traders, a High-Yield Savings Account isn’t just for saving—it’s a critical risk management tool. Mixing your trading capital with your life savings is a recipe for emotional trading and disaster.

- The Rule: At the end of every profitable month, sweep 50% of your trading profits out of your brokerage account.

- The Destination: Move it directly into an FDIC-insured HYSA.

- The Benefit: This locks in your “Alpha” (gains) and transforms risky capital into risk-free passive income (5.00% APY). It prevents the common mistake of “giving it all back” to the market during a drawdown.

Psychological Edge: Knowing your living expenses are growing safely in an HYSA reduces the pressure to force trades, allowing you to trade with a clearer, more disciplined mind.

2. Top High-Interest Savings Accounts for January 2026

Finding the highest yields shouldn’t be complicated. However, the “highest rate” isn’t always the “best account” for everyone. To help you choose quickly, we have categorized the top picks for January 20, 2026 by their specific strengths:

- Best Overall & Large Balances: SoFi (Combines high rates, excellent app UX, and extended FDIC insurance up to $2M).

- Highest APY (Conditional): Varo Bank (Offers the peak 5.00% rate, but requires meeting monthly activity goals).

- Best No-Fee & Simple: Axos Bank (A straightforward, no-nonsense account with zero maintenance fees).

- Best Member-Focused: AdelFi (Ideal for those seeking a values-driven credit union experience).

Detailed Comparison Table

(Rates and terms current as of Jan 20, 2026)

| Institution & Category | APY (Up To) | Min. Deposit / Fees | Why It Wins (Condition & Pros) |

|---|---|---|---|

|

SoFi 🏆 Best Overall Insured by: FDIC (Up to $2M) |

~4.60% | $0 Min $0 Monthly Fee |

Easy to Earn: Requires Direct Deposit for max rate. Top choice for App UX and Large Balances (extended insurance). |

|

Varo Bank 🚀 Highest APY Insured by: FDIC |

5.00% | $0 Min $0 Monthly Fee |

Conditional Rate: Requires direct deposit & debit usage. Best for active spenders chasing the absolute top yield. |

|

Axos Bank 🛡️ Best No-Fee Insured by: FDIC |

~4.60% | $250 to Open $0 Monthly Fee |

Straightforward: No strict hoops to jump through. Perfect for “set it and forget it” savings. |

|

AdelFi Credit Union 🤝 Member Focused Insured by: NCUA |

~5.00% | Low Min No Monthly Fee |

Membership Required: Specific eligibility criteria. Top-tier rate for eligible community members. |

|

Fitness Bank 👟 Best for Habit Insured by: FDIC |

Up to 4.75% | $100 to Open $10 Fee (Waivable) |

Activity Based: Rate tied to daily steps. Unique choice for connecting health & wealth. |

(Disclaimer: APYs are subject to change and may have specific requirements. Information is current as of January 20, 2026 (Investopedia, 2026).Verify directly with the institution.)

3. Current High-Yield Savings Rates & Outlook (Jan 2026)

The gap between a standard bank account and a high-yield account has never been clearer. Switching to a HYSA can essentially multiply your interest earnings by 12x or more without adding risk.

3.1. The Data: National Average vs. Top Yields

According to the most recent FDIC data (January 20, 2026), the national deposit rate for savings accounts is just 0.39%.

- Big Banks: Many traditional “brick-and-mortar” banks still offer as low as 0.01% APY (NerdWallet, 2026)..

- High-Yield Accounts: Leading online platforms (like Varo or AdelFi) offer 4.60% – 5.00% APY.

3.2. The “Conditions” for 5.00% APY

It is important to read the fine print. Accounts offering the headline-grabbing 5.00% APY usually have conditions, such as:

- Direct Deposit: You must deposit a certain amount of salary monthly (e.g., $1,000+).

- Balance Caps: The high rate applies only to the first $5,000 or $10,000.

- Membership: Restricted to specific groups (like AdelFi) or requires active debit card usage.

- Standard HYSA: “No-strings-attached” accounts (like SoFi or Axos) typically settle in the 4.20% – 4.60% range, which is still excellent but slightly below the peak.

3.3. Market Outlook: Will Rates Drop?

As of Q1 2026, interest rates remain elevated but are stabilizing. With inflation moderating, financial analysts suggest that the Federal Reserve may consider gradual rate cuts later this year (Federal Reserve Board, 2026).

- The Move: If you want to lock in these high rates (5%+) for the long term, consider a Certificate of Deposit (CD).

- The Strategy: For savings, simply enjoy the high variable rates now, but be prepared for them to potentially dip slightly to the 4.00% range as the year progresses.

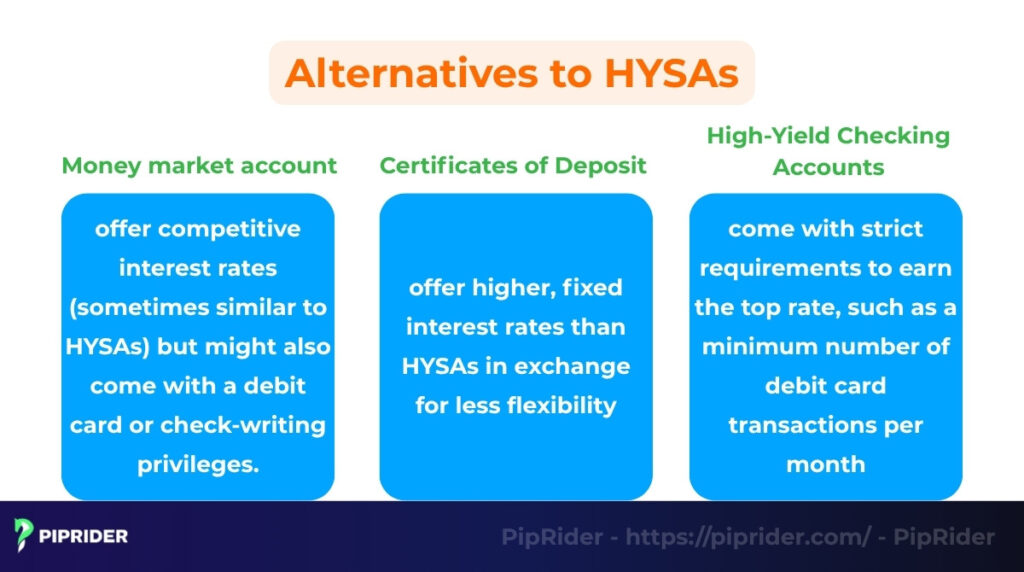

4. Alternatives to High-Yield Savings Accounts

While HYSAs are a great option for earning more on savings, they aren’t the only choice. Depending on your goals for liquidity and return, other deposit accounts might be considered.

4.1. Money market account (MMA)

These accounts often blend features of savings and checking accounts. They typically offer competitive interest rates (sometimes similar to HYSAs) but might also come with a debit card or check-writing privileges.

However, MMAs often require a higher minimum balance than HYSAs and may limit the number of certain types of withdrawals per month. Like HYSAs, they are typically FDIC/NCUA insured.

4.2. Certificates of Deposit (CDs) & Treasury Bills

CDs usually offer higher, fixed interest rates than HYSAs in exchange for less flexibility. When you open a CD, you agree to lock your money away for a specific term (e.g., 6 months, 1 year, 5 years). Withdrawing funds before the term ends usually incurs a penalty.

CDs are also FDIC/NCUA insured and are best for money you know you won’t need immediate access to.

Alternative for Tax Efficiency: U.S. Treasury Bills (T-bills) For savers in high-tax states (like CA or NY), T-bills are often a superior choice to CDs. Backed by the U.S. government, they offer competitive yields similar to HYSAs but with a key advantage: the interest earned is exempt from state and local income taxes (U.S. Department of the Treasury, n.d.).

4.3. High-Yield Checking Accounts

Some banks offer checking accounts with relatively high APYs, sometimes even rivaling HYSAs. However, these accounts often come with strict requirements to earn the top rate, such as a minimum number of debit card transactions per month, direct deposit requirements, or e-statement enrollment.

They are FDIC/NCUA insured but primarily designed for spending, not just saving.

Quick Comparison: Which Account Fits You?

| Account Type | Typical APY | Access (Liquidity) | Risk Level | Insurance |

|---|---|---|---|---|

| High-Yield Savings (HYSA) | High (Variable) | ⭐⭐⭐⭐ Online Transfers |

Very Low | FDIC / NCUA |

| Money Market Acct (MMA) | Moderate – High | ⭐⭐⭐ Checks/Debit Card |

Very Low | FDIC / NCUA |

| Certificate of Deposit (CD) | Highest (Fixed) | ⭐ Locked for Term |

Very Low | FDIC / NCUA |

| Treasury Bills (T-bills) | High (Fixed) | ⭐⭐ Short Term Lock |

Zero Risk | US Gov Backed |

Key takeaway: HYSAs generally offer the best combination of high (though variable) interest rates and easy access to your funds among low-risk savings options.

5. Benefits and Drawbacks of High-Interest Savings Accounts

While saver accounts high interest options are appealing, it’s wise to weigh their advantages against potential downsides before deciding if they’re right for your banking needs.

5.1. Pros (Advantages)

These accounts offer several compelling benefits for savers.

- Higher earnings & safety: The primary benefit is the significantly higher interest rate (APY) compared to traditional savings accounts, allowing your money to grow faster. Plus, funds are typically FDIC or NCUA insured, making them very safe.

- Easy access (Liquidity): Unlike Certificates of Deposit (CDs), your money in an HYSA is usually readily accessible. You can typically withdraw or transfer funds online or via a mobile app when needed.

- Suitability for specific goals: Their combination of safety, decent returns, and accessibility makes HYSAs perfect for emergency funds or saving for short-to-medium-term goals like a down payment or vacation. Additionally, using a savings buffer to reduce trading pressure can provide the psychological stability needed for better financial discipline.

5.2. Cons (Disadvantages)

Consider these potential drawbacks before opening an account.

- Variable interest rates: The high APY offered by HYSAs is variable, meaning it can go up or down based on market conditions and Federal Reserve rate changes. Rates are not locked in like CDs.

- Limited physical access: Many of the banks offering the best rates are online-only. This means there are no physical branches for in-person banking or cash deposits.

- Potential Withdrawal Limits (Regulation D): Historically, Federal Regulation D capped “convenient” withdrawals at 6 per month. Although the Federal Reserve indefinitely removed this limit in 2020, many banks still voluntarily enforce it as an internal policy. Exceeding this limit at some institutions can still result in “excess withdrawal fees” or account conversion.

6. How Much Can You Earn with a High-Interest Savings Account?

The main appeal of a high-yield savings account is its ability to significantly boost your earnings compared to traditional savings. But how much difference does it really make? The key lies in understanding the Annual Percentage Yield (APY) and the power of compound interest.

Understanding APY (Annual Percentage Yield)

APY represents the total amount of interest you will earn on a deposit account over one year, including the effect of compound interest. Unlike a simple interest rate, APY reflects the interest earned on your initial deposit plus the interest earned on the accumulated interest.

Banks usually compound interest daily or monthly, which slightly increases your effective return over time. A good APY for savings account is one significantly higher than the national average.

The Power of Compound Interest

Compound interest means your interest earns interest. Even small amounts add up over time, especially with a higher APY. The more frequently interest is compounded (e.g., daily vs. annually), the faster your money grows.

Earning Examples (Annual Earnings)

Let’s see how much you could potentially earn in one year with different balances, assuming competitive APYs available around January 2026:

- With $1,000 Saved:

- At 4.50% APY: You could earn approximately $45.

- At 5.00% APY: You could earn approximately $50.

- With $5,000 Saved:

- At 4.50% APY: You could earn approximately $225.

- At 5.00% APY: You could earn approximately $250.

- With $10,000 Saved:

- At 4.50% APY: You could earn approximately $450.

- At 5.00% APY: You could earn approximately $500.

Compare this to a traditional savings account earning maybe 0.40% APY, where $10,000 would only earn $40 in a year. The difference highlights why seeking out the best interest rates on deposit accounts is worthwhile.

7. How to Choose a High-Yield Savings Account

To choose the best high-yield savings account (HYSA), you must evaluate more than just the advertised interest rate. The ideal account offers a balance of high APY, zero fees, reasonable minimum requirements, and fast access to funds. Use the following checklist to vet any account before applying.

7.1. APY Tiers & Balance Caps

Check if the high rate applies to your entire deposit. Some banks use a “tiered” interest structure, where the advertised 5.00% APY only applies to the first $5,000 or $10,000. Balances exceeding that limit may earn a significantly lower rate (often 0.50% or less). Always calculate the blended APY for your total intended deposit amount.

7.2. Requirements to Earn Top APY

Identify the “hoops” you must jump through to get the maximum rate. Accounts offering rates significantly above the market average often come with strict conditions. To unlock the headline APY, you may need to:

- Set up recurring Direct Deposits (e.g., $1,000+ monthly).

- Perform a minimum number of debit card transactions (e.g., 10 swipes per month).

- Verdict: If you cannot consistently meet these criteria, a “no-strings-attached” account with a slightly lower rate is often the smarter financial choice.

7.3. Fees & Minimum Balance

Ensure monthly fees do not eat into your interest earnings. A true high-yield savings account should generally charge $0 monthly maintenance fees.

- Monthly Fees: Avoid accounts that charge a fee unless you maintain a high minimum balance.

- Minimum Opening Deposit: While many top online banks allow you to open an account with $0, some may require an initial deposit of $100 or $250.

7.4. Transfer Speed and Liquidity

The time required to move funds is a critical factor for managing active capital. While HYSAs provide high growth, fund accessibility varies depending on the institution’s infrastructure.

- Standard ACH: Most electronic transfers settle within 1 to 3 business days, depending on the banks’ processing cycles.

- Faster Access: Features like Same-Day ACH, Zelle, or internal bank transfers can significantly reduce transit time during market opportunities.

- Limits: Always review bank-specific transfer caps and settlement policies to ensure the account’s liquidity meets your specific requirements.

7.5. Safety Verification (FDIC/NCUA)

Never compromise on federal insurance coverage. Before depositing funds, verify the institution’s safety status to ensure you are protected up to $250,000 per depositor (FDIC, n.d.).

- For Banks: Look for FDIC (Federal Deposit Insurance Corp) membership.

- For Credit Unions: Look for NCUA (National Credit Union Administration) insurance.

Action: Verify the institution directly on the official FDIC BankFind or NCUA Locator websites.

8. Are High-Interest Savings Accounts Safe?

Yes, a high-yield savings account from a legitimate U.S. bank or credit union is very safe.

Deposit Insurance

Your funds are typically protected by FDIC insurance (for banks) or NCUA insurance (for credit unions), which insures you up to $250,000 per depositor, per institution. This protects your money if the institution fails. This guaranteed safety is a stark contrast to more aggressive financing methods, where understanding the risks of using home equity for investing or trading is crucial to avoid putting your primary residence at risk.

“Member FDIC” vs. Partnered Insurance

- “Member FDIC” means the bank itself is insured.

- Wording like “Funds insured by FDIC” (often seen with fintech apps) means your money is held at partner banks that are FDIC-insured. While generally safe, know where your money is held to stay within insurance limits if using multiple apps linked to the same partner bank.

Online Bank Safety

Online banks offering the best interest rates on deposit accounts are just as safe as traditional banks, provided they are FDIC or NCUA insured. Always verify their insurance status and check for strong online security features.

9. Taxes and Account Maintenance

Earning high interest also comes with a few responsibilities.

9.1. Taxes on Interest Income

Interest earned from savings accounts (including HYSAs) is considered taxable income by the IRS.

Your bank or credit union will typically send you Form 1099-INT early in the year if you earned $10 or more in interest. You must report this interest income when you file your federal and potentially state income taxes.

9.2. Maintaining High APY Eligibility

Some banks high yield savings account options require specific actions to earn the highest advertised APY. Common requirements include:

- Maintaining a minimum balance (though many top HYSAs don’t have this).

- Setting up qualifying direct deposits.

- Meeting a minimum number of debit card transactions per month (more common for high-yield checking).

Always read the account terms carefully to understand how to keep earning the best savings yields.

Once you’ve maxed out the benefits of HYSAs, exchange traded funds as a next step beyond savings can help grow wealth faster. Just make sure your emergency fund stays protected first.

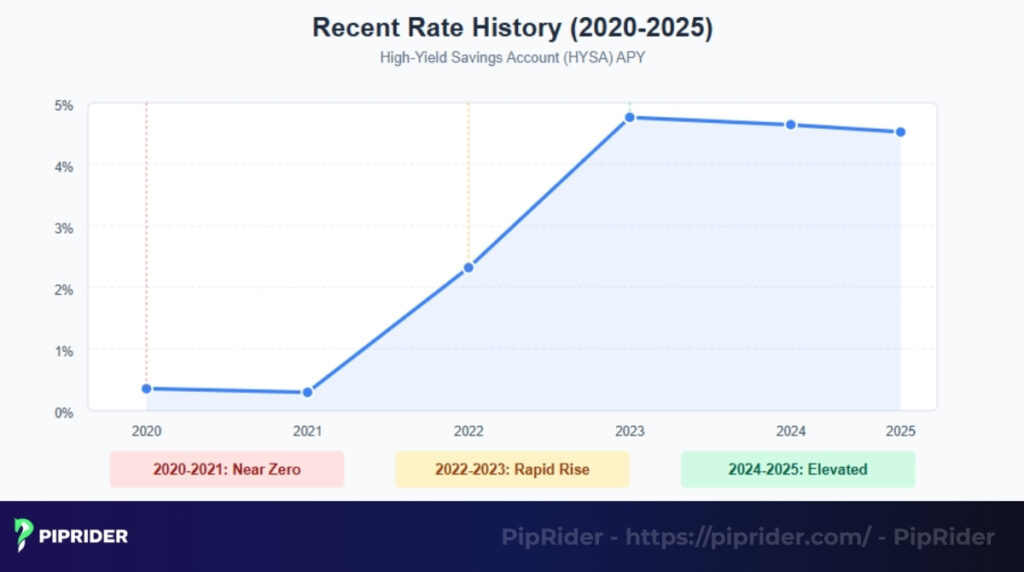

10. Historical Interest Rates & Trends

High yield rate savings account APYs are not static; they fluctuate significantly over time, largely mirroring broader economic trends and central bank policy.

10.1. Recent Rate History (2020–2026)

- 2020-2021: Following the economic shock of the pandemic, the Federal Reserve cut the Fed Funds Rate to near zero. Consequently, APYs on even the best HYSAs plummeted, often falling well below 1%.

- 2022-2023: As inflation surged, the Fed embarked on an aggressive rate-hiking cycle. Banks quickly followed suit, pushing HYSA rates rapidly higher, eventually exceeding 4% and even 5% in some cases.

- 2024-Present (Jan 2026): Rates have largely remained elevated, with top accounts offering near 5.00% APY, though markets are watching closely for potential policy shifts in 2026.

10.2. Key Drivers: Fed Funds Rate and Inflation

The Federal Funds Rate is the primary driver of savings account yields. Banks typically adjust their deposit rates in response to changes (or expected changes) in the Fed’s target rate.

Inflation also plays a crucial role, as the Fed raises rates to combat high inflation and may cut rates when inflation falls significantly below target.

10.3. Short-Term Outlook (2026)

As discussed earlier, with inflation moderating, the market anticipates potential rate adjustments. This suggests that while still attractive, the peak best savings yields seen recently might slowly decline through the remainder of 2026, though they are expected to stay well above traditional savings rates.

11. Frequently asked questions about Saver Accounts High Interest Rates

12. Methodology

The information and Annual Percentage Yields (APYs) in this guide, particularly in the “Top High-Interest Savings Accounts” section, are based on compiled data. This data was sourced from leading financial comparison and review websites such as NerdWallet, Bankrate, and Investopedia, reflecting rates available as of Jan 2026.

Our evaluation and selection process prioritized the following key criteria:

- Competitive APY: Identifying accounts offering significantly higher rates than the national average.

- Low or No Fees: Favoring accounts with no monthly maintenance fees and minimal incidental charges.

- Account Requirements: Considering minimum deposit/balance requirements and any conditions needed to earn the top APY.

- Safety and Reliability: Ensuring the institutions are insured by the FDIC or NCUA.

13. The Bottom Line

High-interest savings accounts, often the best saver accounts high interest options available, offer a safe and effective way to make your idle cash work harder, providing much better returns than traditional savings options. They are ideal for individuals looking to preserve capital while maximizing short-term earnings on funds like emergency savings or down payments.

To get the most benefit, it’s crucial to compare APYs and account features regularly and always choose an institution insured by the FDIC or NCUA.

Follow PipRider and our Broker Reviews section to stay updated with more insights and knowledge to manage your finances effectively.