To calculate the Average Daily Range (ADR), you find the average of the simple (High – Low) range of an asset over a set period, like 14 days. Unlike the ATR, the ADR ignores overnight gaps, making it a popular volatility tool for day traders.

This guide explains how to calculate the ADR indicator with a simple formula and details the critical differences between ADR vs. ATR. Piprider also shows how to use this metric to set daily profit targets and stop-loss levels.

Key Takeaways

- The Average Daily Range (ADR) is an indicator that shows an asset’s average (High-Low) price movement for one day.

- It is calculated by averaging the daily price range(Daily High – Daily Low) over a set period (e.g., 5-14 days).

- ADR vs. ATR: The key difference is that ADR ignores overnight gaps, while the ATR indicator (Average True Range) includes gaps.

- Day traders use the ADR to set realistic daily profit targets (e.g., 80% of the ADR) and to place stop-loss orders outside of the normal “noise.”

- A common trading strategy is to identify “overextended” moves. If the price has already moved 100% of its ADR, it is less likely to continue in that direction.

1. What Is the Average Daily Range (ADR)?

The Average Daily Range (ADR) is a simple indicator that measures the average distance an asset’s price moves between its high and low on a typical day. It is usually calculated over the last 5 to 14 days.

For traders, the ADR indicator is a powerful volatility tool. It helps them set realistic expectations for how far the price might move in a single day. This information is crucial for:

- Setting logical take-profit targets.

- Placing stop-loss orders outside of the expected daily “noise.”

- Identifying if a market is in a low-volatility (sideways) or high-volatility (trending) state.

The ADR is often confused with the ATR indicator (Average True Range), but there is one critical difference: the ADR ignores overnight gaps and only measures the (High – Low) of the day. The ATR, however, includes gaps in its calculation.

2. Why Does the ADR Matter in Trading?

The ADR matters because it gives you a data-driven map of a normal trading day, especially in the Forex market. Instead of guessing, you get a clear statistical average for how far a price is likely to move, which is critical for making good decisions.

- Measuring the natural daily price range of a stock or forex pair helps you understand its unique personality.

- The ADR indicator helps you avoid “chasing” a trade. If the price has already moved beyond its average daily range, entering a new trade in that same direction is very high-risk.

- Providing a logical basis for setting Stop-Loss (SL) and Take-Profit (TP) levels is the ADR’s most popular use.

- This tool also helps traders identify market conditions. A very low ADR signals a quiet, “sideways” market, while a rising ADR signals a “trending” market with high volatility.

3. How to Calculate the ADR Indicator? (Formula and Example)

Learning how to calculate the adr indicator involves taking a simple average of the daily (High – Low) range over a set number of days.

Unlike the ATR, this formula ignores overnight gaps, making it a “cleaner” measure of a single day’s expected volatility for technical analysis.

3.1. The ADR Formula

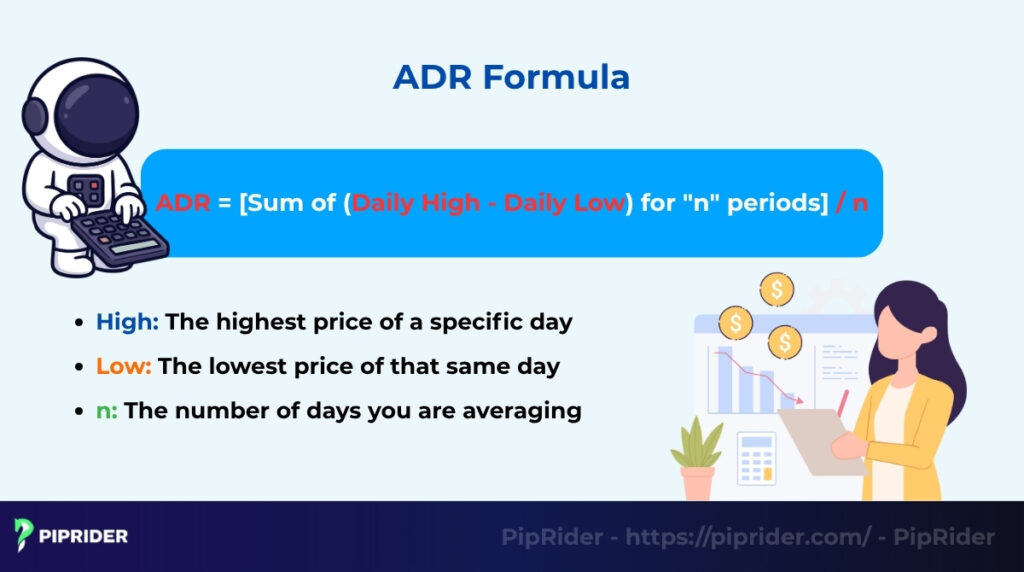

The formula for the Average Daily Range in plain text is:

ADR = [Sum of (Daily High – Daily Low) for “n” periods] / n

- High: The highest price of a specific day.

- Low: The lowest price of that same day.

- n: The number of days you are averaging (a 14-day period is common, but some day traders use 5 or 10).

3.2. Step-by-Step Example

You don’t need to do this math manually (the ADR indicator does it for you), but here is how the calculation works for a 14-day period.

- You get the High and Low price for each of the last 14 trading days.

- For each day, you find the range: (High – Low).

- You add up the ranges for all 14 days.

- You divide that total by 14.

Example (EUR/USD):

- Total of the last 14 daily ranges = 1,260 pips

- ADR(14) = 1,260 pips / 14

- ADR = 90 pips

This 90-pip value tells you that over the last 14 days, EUR/USD has moved an average of 90 pips between its high and low.

3.3. ADR vs. ATR: The Key Differences

The most important question traders ask is how the ADR compares to the ATR indicator (Average True Range). The main difference is that ADR ignores gaps.

| Factor | Average Daily Range (ADR) | Average True Range (ATR) |

| Gaps Included? | No | Yes |

| Primary Use Case | Measures a single session’s average range. | Measures overall volatility, including gaps. |

| Common Period | 5–14 days | 14 days |

| Best For | Intraday (Day) Traders | All traders, including swing/position. |

4. How Do You Use the ADR in Trading?

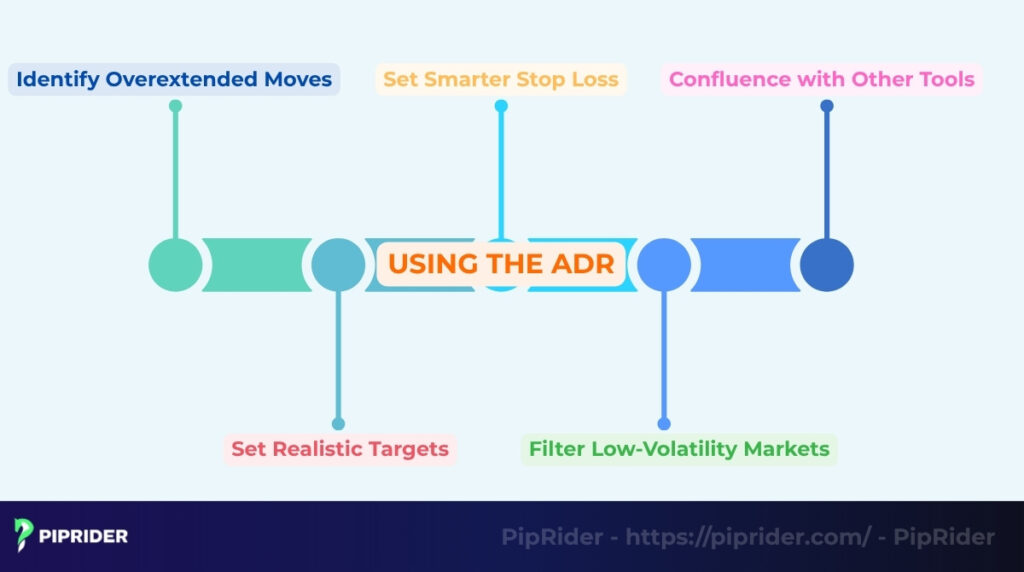

The Average Daily Range’s real value is in its application for day trading. You can use it to identify overextended moves, set logical profit targets and stop-losses, filter low-volatility markets, and confirm signals with other indicators.

4.1. Identify Overextended Moves

A primary use of the ADR is to identify “overextended” moves. If an asset’s price has already moved the full 100% of its ADR for the day, the tank is likely “empty.” Chasing a trade in that same direction is high-risk because the probability of a reversal or a stall is much higher.

4.2. Set Realistic Targets

The ADR is excellent for setting realistic take-profit (TP) targets. If the 14-day ADR is 100 pips, expecting a 200-pip move in one day is unrealistic. Many day traders will look for major resistance levels that fall within 70% to 90% of the ADR value (e.g., 70-90 pips from the daily open if the ADR is 100) to set their final TP.

4.3. Set Smarter Stop Loss

Instead of using a fixed 20-pip stop on every trade, you can set a “smarter” stop-loss based on the Average Daily Range. A stop-loss should be a percentage of the volatility. For example, a common stop-loss might be 25-30% of the ADR value (e.g., 25-30 pips if the ADR is 100). This adapts your risk to the market’s current volatility.

4.4. Filter Low-Volatility Markets

The Average Daily Range value helps you filter which markets to trade. If a pair’s ADR is very low (e.g., under 50 pips for a major pair), the market is in a tight, “sideways” range. This is a poor environment for breakout strategies, and you might avoid trading that asset.

4.5. Confluence with Other Tools

The ADR works best when used in confluence with other technical indicators and price action. For example, if a price hits the 100% ADR level at the same time it hits a major resistance zone, the signal for a reversal is much stronger. It can be combined with:

- Support and resistance levels

- Moving Averages (EMA50, EMA200)

- Volatility tools like Bollinger Bands

5. What Are Some ADR Trading Strategies?

You can build specific Forex trading strategies around the Average Daily Range value. Most strategies focus on either the price breaking its daily price range on a strong trend day or reversing from the edge of it.

5.1. The ADR Breakout Strategy

A breakout strategy assumes the day will be a strong trend day. The entry signal occurs when the price breaks beyond 100% of the ADR range, usually during the high-volume London or New York sessions.

- Confirmation: This move must be confirmed by a strong increase in volume or a clear price action signal like a market structure shift (MSS).

- SL/TP: A trader might set a Take Profit (TP) at 1.2x the ADR and a Stop-Loss (SL) at 0.5x the ADR, betting on continued momentum.

5.2. The ADR Reversion Strategy

A mean-reversion strategy works on the opposite idea. It assumes the price is “overextended” and will pull back.

- The Setup: When the price stretches to 110% or 120% of the ADR, reversion traders stop looking for trades in that direction.

- The Entry: They look for price action reversal signals (like a pin bar or engulfing candle) to trade against the move, back toward the average. This is popular for scalping setups.

5.3. ADR with Supply and Demand

Combining the ADR indicator with Supply and Demand zones uses the ADR as a “fuel gauge.”

- The setup: For example, the price pulls back to a strong demand zone (a good place to buy).

- The entry: Before buying, you check the ADR. If the price has not yet reached its full ADR limit for the day, it signals there is still “room to move up,” making the buy trade a higher-probability setup.

6. What Tools and Indicators Calculate the ADR?

You do not need to calculate the ADR manually. Most traders use an indicator on their trading platform (like MT4, MT5, or TradingView) or a simple spreadsheet.

6.1. ADR Indicator for MT4/MT5

Since the ADR is not a default indicator, you will need to find a custom ADR indicator for MT4 or MT5. These are widely available online. A good indicator will automatically:

- Display the ADR values (e.g., ADR(5), ADR(10), ADR(14)).

- Plot the projected daily high and low levels based on the ADR.

- Often include an alert feature to notify you when the price hits 100% of the ADR range. This allows you to test your strategies in MT4 more effectively by observing how price reacts to these levels over time.

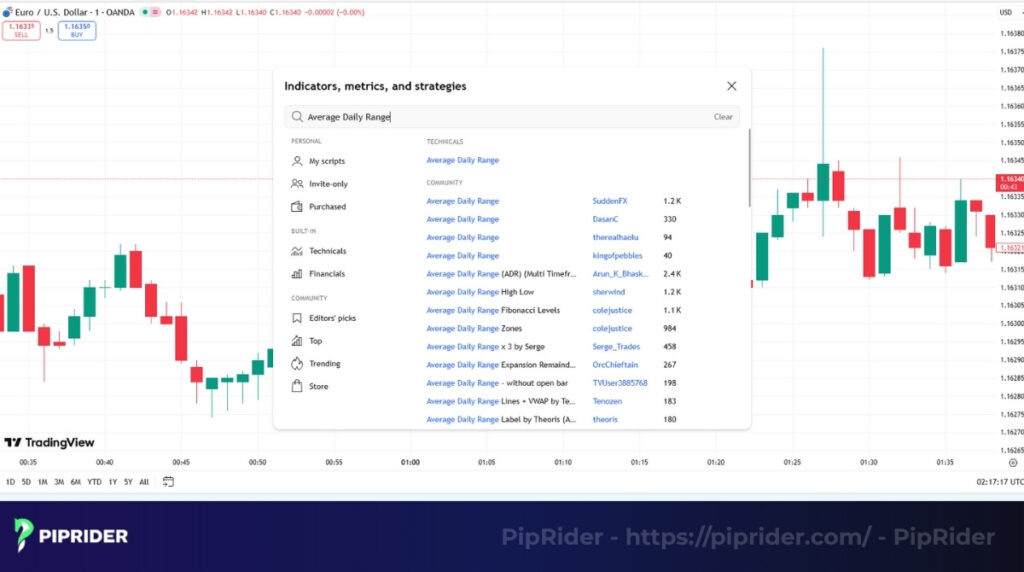

6.2. TradingView ADR Tools

TradingView has many ADR tools available in its public “Community Scripts” library. You can search for “Average Daily Range” to find them.

- Many of these Pine Script indicators will overlay the ADR range directly onto your chart, showing you the projected daily high and low as colored lines, which makes it very easy to see.

6.3. Manual Calculation via Excel

If you prefer to learn how to calculate the adr indicator manually, you can easily do it in Excel.

- Download the daily OHLC (Open, High, Low, Close) data from your MT4 or TradingView platform.

- Create a new column for “Range” and apply the formula: (High – Low).

- Use the AVERAGE function in Excel to apply the ADR formula: =AVERAGE(Range_Column) over your chosen period (e.g., the last 14 cells).

7. What Is an Example of Using ADR on EUR/USD?

Here is a simplified example of how the ADR(14) for EUR/USD is calculated and then applied to a trading decision.

First, a trader looks at the last 14 days of data to find the daily range.

| Day | High | Low | Range (pips) |

| 1 | 1.0940 | 1.0850 | 90 |

| 2 | 1.0965 | 1.0875 | 90 |

| 3 | 1.0980 | 1.0890 | 90 |

| … | … | … | … |

| 14 | … | … | … |

| 14-Day Total | — | — | 1260 pips |

| ADR(14) | — | — | 90 pips (1260 / 14) |

The resulting ADR(14) value is 90 pips. A day trader will now use this value for the current trading day.

Example Application:

- A strong uptrend is visible on the M15 chart.

- Before placing a buy order, a trader checks how far the price movements have gone today (from the daily low to the current high).

- The price is observed to have already moved 85 pips.

- Decision: Since 85 pips is very close to the 90-pip average, the market is likely “overextended.” A new buy trade should be avoided because the probability of a reversal or a stall is high. This is a key part of how to calculate the adr indicator‘s practical use.

8. What Are the Common Mistakes When Using ADR?

The most common mistake is using the ADR mechanically without understanding the market context. Traders often confuse the ADR indicator with the ATR or IR indicator, use the wrong timeframe, or fail to combine it with other signals.

- Using the wrong timeframe: The Average Daily Range (ADR) measures the range for the entire day. Applying this 90-pip range to a 5-minute “scalping” trade is not appropriate and can lead to losses.

- Not updating data: Markets change. Last week’s 90-pip ADR might not be accurate this week (e.g., after major news). If the data isn’t fresh, your range won’t reflect the current volatility.

- Confusing ADR with ATR: The biggest error is confusing ADR with ATR. If your strategy needs to account for overnight gaps, you must use the ATR. Using the ADR in that case might cause you to set your stop-loss too tight.

- Not combining with other factors: The ADR is not a complete trading system. A mistake is to rely only on the ADR without combining it with other key technical analysis factors like volume, market structure, and session volatility.

9. Frequently asked questions about Calculating the ADR Indicator

10. Conclusion

The Average Daily Range (ADR) is a simple but powerful tool. Learning how to calculate the ADR indicator helps a trader measure the average volatility. This metric is essential for setting logical stop-loss and take-profit levels and filtering trading signals.

Understanding the ADR means you understand the market’s “rhythm”, a vital skill for any professional trader. For maximum effectiveness, always use the ADR indicator in combination with market structure, price action, volume, and session timing.

To learn more expert trading strategies and improve your analysis, explore the free guides at Piprider.